This post is part of Gallup's ongoing series on the shifting landscape for financial institutions. It provides insights into channel optimization, emerging customer behaviors and preferences, product penetration and relationship growth, engaging the most critical affluent and business customers, and reshaping banks' overall value proposition.

Time and again, our clients tell us that solving customer problems is critical to their business. The impetus for their concern is largely regulatory and rightfully so, as most banks are concerned with CPFB compliance. But the impact of problem resolution -- or lack thereof -- on customer engagement and overall customer relationship management should not be underestimated.

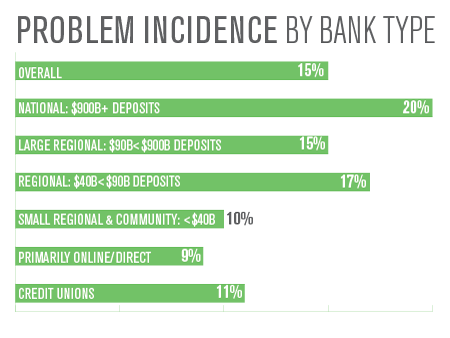

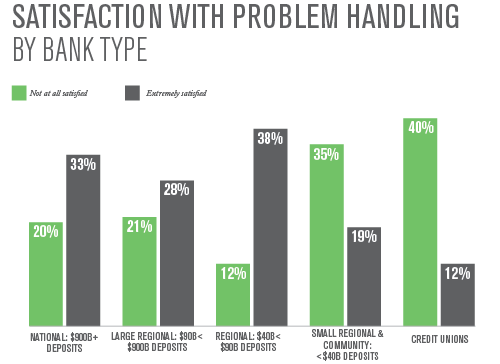

The latest Gallup research on retail banking shows that, on average, 15% of customers have experienced a problem with their bank in the past six months. Only 24% are extremely satisfied with the problem resolution they received, while 27% are not at all satisfied.

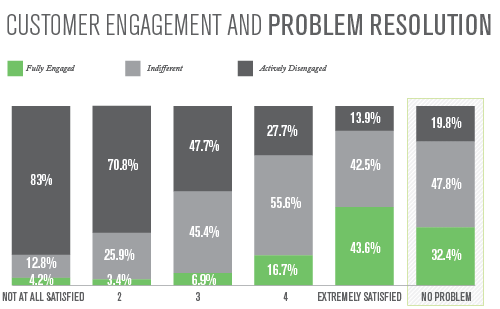

While customers' lack of satisfaction with problem resolution has many causes and many solutions, it has one outsized impact on a bank's business -- it significantly lowers their customer engagement. In fact, banks can't just "satisfy" customers through problem resolution, they need to perform at extremely high levels to get engagement back to that of a customer who had no problem. When banks go above and beyond, they are rewarded. Gallup has discovered that customers who are extremely satisfied with the way their problem was handled actually become more engaged than customers who did not report a problem (44% fully engaged vs. 32% fully engaged).

Customer engagement is a financial imperative for banks. When customers have a problem, banks are presented with a critical moment of truth that will impact their overall relationship and engagement with those customers. Banks must get problem resolution right, or they risk alienating their customers and diminishing their revenue. Almost one-third of banking customers are extremely unsatisfied with the way their bank handles problem resolution. For any industry, that number is high, and for one as personal as finance, it is completely unacceptable.

Bank Size Definitions:

National: $500B+ deposits

Large Regional: $90B+ deposits

Regional $40-99B in deposits

Small Regional & Community: <$40B in deposits

Online/Direct: No significant physical presence (e.g., USAA, Schwab, E*TRADE, Ally)

Credit Union: Chartered Credit Unions