Story Highlights

- 80% of retirees have ample retirement money; 53% of nonretirees expect to

- Retirees more reliant on Social Security than nonretirees plan to be

- Nonretirees most likely to think 401(k) will be major retirement income source

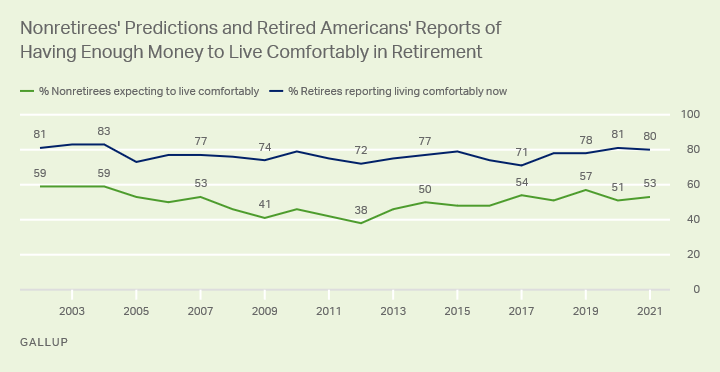

WASHINGTON, D.C. -- The vast majority of U.S. retirees report having enough money to live comfortably; 80% say so today. At the same time, far fewer nonretirees, 53%, expect to have enough money to live comfortably when they retire. The economic fallout from the coronavirus has done little to alter these views, especially in comparison to the much more notable downturn in nonretirees' expectations during and immediately after the 2007-2009 Great Recession.

Line chart. Retired Americans' reports that they have enough money to live comfortably now and nonretired Americans' expectations that they will have enough money to live comfortably when they retire, trend since 2002. Currently, 80% of retirees say they have enough money and 53% of nonretirees think they will have enough money.

In April 2020, amid widespread business closures and a nearly 15% national unemployment rate, 51% of nonretired Americans said they thought they would have enough money to fund their retirement adequately, a six-percentage-point drop from the previous year. Nonretirees' expectations remain more pessimistic today than immediately before the pandemic.

The same pattern is not seen among retired U.S. adults, however, as steady, broad majorities reported they were living comfortably despite the economic upheaval of the past two years. Retirees' reports of their financial situation were also largely unaffected by the Great Recession.

The latest data are from Gallup's annual Economy and Personal Finance survey, conducted April 1-21. Since 2002, majorities of retirees ranging between 71% and 83% have said they have enough money to live comfortably. Over the same period, far fewer of those not yet retired (from 38% to 59%) have anticipated a similar outcome for themselves. It is unclear if these differences result from retirees being better prepared financially for retirement than today's nonretirees are, or if nonretirees are overly pessimistic about what their retirement finances will look like.

Nonretirees' Expectations of Retirement Vary by Income

As has been the case in the past, expectations of retirement among nonretirees differ based on income level. Those with higher incomes are most likely to forecast a comfortable retirement for themselves.

| Yes | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Annual household income | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Less than $40,000 | 33 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $40,000-<$100,000 | 49 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $100,000 or more | 75 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| GALLUP, APRIL 1-21, 2021 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

There are no meaningful differences by age in the current survey, although in the past, younger adults have often been more confident than their older counterparts when it comes to nonretirees' outlooks for a comfortable retirement.

Expectations of Nonretirees vs. Reality of Retirees

Disparities between nonretirees' expectations and retirees' actual experiences are also evident in their reports of retirement income sources and retirement ages.

The differences in reliance on income sources between those who are already retired and those who are not yet retired are likely attributable, at least in part, to apprehension about the Social Security system, as well as the rise of 401(k)s accompanied by a decline in work-sponsored pension plans.

-

57% of retired U.S. adults say they rely on Social Security as a major income source, and 38% of nonretirees expect it to be a major source for them.

-

Likewise, 36% of retirees and 19% of nonretirees say a work-sponsored pension plan is or will be a major income source.

-

Nonretirees are most likely to say a 401(k) or other retirement savings account will fund their retirement (49%). Meanwhile, 35% of retirees mention 401(k)s as a major funding source of their retirement.

Nonretirees are also more likely than their retired counterparts to say they (will) rely on several other income sources to at least a minor degree, including other savings accounts, home equity, part-time work, rent and royalties, and inheritance money. There is less divergence in viewing annuities or insurance plans or individual stock or stock mutual fund investments as an income source.

Bar graph. Nonretirees' views of how significant each of 10 income sources will be to them in their retirement plus retirees' reports of how much of a source each currently is. Fifty-seven percent of retirees say Social Security is a major source of retirement income, but fewer nonretirees, 38%, think it will be. Nonretirees are most likely to say a 401(k) or other retirement savings account will fund their retirement (49%), while 35% of retirees mention them as a major funding source of their retirement.

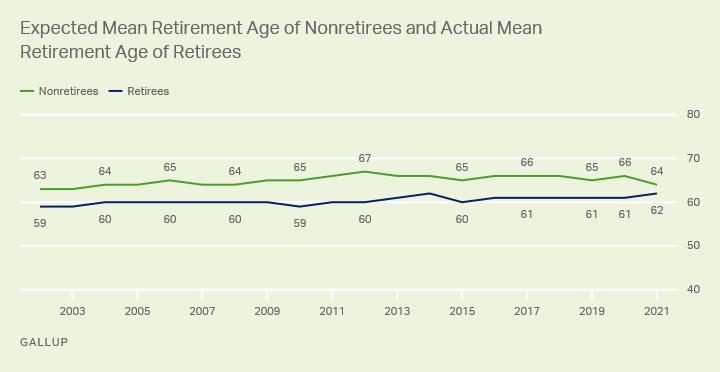

In addition to income sources, retirement age is another area of discrepancy between those who are already retired and those who are not retired. Since 2002, the mean age at which retirees report they stopped working has been modestly lower than the mean age at which nonretirees predict they will retire. The latest survey finds the actual mean retirement age for retirees was 62, while the mean expected retirement age for nonretirees is 64. These readings are in line with previous findings.

Line graph. Expected mean retirement age of nonretirees and reported mean retirement age of retired U.S. adults, trend since 2002. Currently, the mean age of retirement among retirees is 62 years old and the mean expected retirement age of nonretirees is 64.

Again, it is unclear why the discrepancies exist. With the age at which people can receive Social Security benefits higher for retirees today than in the past, many nonretirees may be looking to delay retirement to a later age than today's retirees did. However, it is also possible that nonretirees' plans will be altered by their employers' staffing plans, their physical health or job market conditions, forcing them to retire before they ideally would like to.

Bottom Line

Although not having enough money for retirement is Americans' top financial concern, with nearly three in five saying they are worried about having enough money for retirement, a slim majority of nonretirees in the U.S. expect they will have enough money to live comfortably in their retirement. And a large majority of retired U.S. adults say they are now living comfortably. Given the decline in employer-sponsored pensions and questions about Social Security's future, those who are not yet retired may simply be more concerned about a lack of reliable retirement income.

View complete question responses and trends (PDF download).

Learn more about how the Gallup Poll Social Series works.