As bankers, you know a lot about your customers. You know their demographic data, their transaction activity, and their financial history. You are likely to know every necessary personal detail that will protect your assets and improve theirs. But do your customers know you?

It's difficult to understand why bankers aren't working to reap the benefits that come from deeper relationships with their customers.

For the most part, they don't. At least, that's what a recent Gallup Panel study discovered. Gallup surveyed more than 38,000 customers of more than 175 financial institutions throughout the United States and asked them: "Do you have a particular employee (like a teller or manager) who you like to work with at [your] bank or financial services company?" At some of those institutions, including banks and credit unions, 60% or more of the customers could answer yes to that question.

But I was disappointed to learn that overall, less than 35% of the customers surveyed said they had a particular employee they liked to work with at their bank. At the same time, the survey results revealed that 94% of customers use the branch channel, and 67% visit at least once a month. (See "Where Do People Do Their Banking?" in the "See Also" area on this page.)

One would think that when a customer has regular interaction with a bank's personnel, he or she would create a relationship with at least one employee, but evidently that's not happening. This indicates that banks are missing a prime opportunity to engage their customers. It also suggests that many banks aren't fulfilling their brand promise. In their advertising, financial services companies regularly tell consumers that "your local banker" is "involved," "committed to your success," and a "critical part of the community." Yet according to our research, these same bankers are just as likely to be a mystery to many of their customers.

Maintaining banker anonymity may be a conscious choice for some banks -- and there is certainly a point to be made about the bank or brand being bigger than any particular person. But it's difficult to understand why bankers aren't working to reap the benefits that come from deeper relationships with their customers.

Customer engagement: the bottom line

Why should you care if your customer knows someone at the bank? Well, for one thing, the same Gallup survey revealed that 51% of banking customers preferred using the branch channel. That's the channel customers use most often, so that's where the bank should focus its customer engagement efforts. Further, branches are the most expensive of all customer interfaces, so banks need to maximize their return from that investment. But the most important reason you should care is because "knowing someone at the bank" is the first step toward creating deeper relationships and customer engagement.

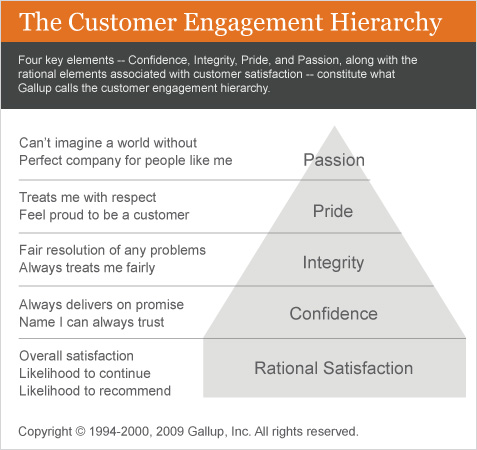

Gallup has been studying customer engagement -- a powerful emotional attachment to a brand or product -- for almost a decade. The baseline requirement for customer engagement is rational satisfaction, which comes from satisfying a customer's basic needs, such as price, speed, and efficiency. Companies that fulfill these needs will have customers who are more likely to be loyal, to recommend the company to others, and to continue being a customer. A real difference in customer behavior -- and profitability -- comes from going beyond rational satisfaction to emotionally engaging customers with your products and services. (See "Customer Satisfaction: A Flawed Measure" in the "See Also" area on this page.)

Gallup has found that customer engagement is based on four hierarchical needs beyond rational satisfaction. The first level is Confidence, the belief that the company or brand always delivers on its promises and is a name that customers can always trust. The second element is Integrity, which reflects the belief that the company always treats its customers fairly and resolves problems fairly. Next is Pride, the degree to which customers feel that the company respects them and the level of pride they feel about their association with the company. The top of the hierarchy is Passion. Passionate customers say that the company is "perfect for people like me" and that they "can't imagine a world without" it. (See graphic "The Customer Engagement Hierarchy.")

Rational satisfaction must be met first, of course, because that's the baseline expectation. But as banks fulfill each need after that, they inspire more and more customer engagement. They also reach a higher pinnacle of profitability. Fully engaged customers deliver a 23% premium over average customers in share of wallet, profitability, revenue, and relationship growth, while actively disengaged customers represent a 13% discount on the same measures, according to Gallup research.

There's more. A business impact analysis of customer engagement for a large regional bank showed that among repeat customers who had visited a branch location twice and interacted with a branch associate on both visits:

-

fully engaged customers increased their account balances by 9%

-

customers who moved from disengaged to fully engaged increased their account balances by 12%

-

customers who moved from fully engaged to disengaged decreased their account balances by 7%

-

customers who were disengaged following both visits decreased their account balances by 8%

What the customer wants

One of the most important discoveries that Gallup researchers have made is that if you want to create excellence, you should study excellence. In other words, you can learn a lot more about being the best from the best in any given category than you can learn from the worst.

With that in mind, Gallup took a close look at the 35% of customers who say they have a particular employee they like to work with at their bank. Specifically, we wanted to explore what was driving the relationship. We wanted to know what those individual bank employees were doing from a customer's perspective and how they were making the customers feel. Gallup did this by ranking bank employees based on whether their customers strongly agreed with several statements. (See graphic "Building Relationships With Customers.")

Notice that the banking employees who are successfully building relationships with customers are doing many of the basics right. Their customers perceive them as trustworthy, they follow through on their actions, and they do things right the first time. But when it comes to things that will keep customers coming back -- understanding customers' financial goals, keeping customers informed of new opportunities, making customers proud of where they bank, and going out of their way to please customers -- only about half of customers can strongly agree that these bank employees are performing these actions.

And what about the 65% of customers who haven't established a relationship with a particular employee at their bank, even though a majority of all customers visit a branch at least once a month? For these customers, it's likely that bank employees aren't memorable because they aren't sparking an emotional connection. And that's probably because bank employees don't realize how important that emotional connection is to customer engagement. That's a shame -- and a lost opportunity. A bank's engaged customers could become early adopters of new and profitable services. And ultimately, they could become the best brand ambassadors if they had a trusted advisor at their bank.

Is your whole team playing?

According to the FDIC, as of September 2008, there were just over 2.1 million full-time employees working in FDIC-insured banks. Yet based on their responses, customers have built relationships with just over 700,000 of these bank employees.

At some point, every one of your bank's customers will need advice, guidance, or a product to help them reach their financial goals. The customers who don't have a relationship with someone at your bank won't feel like they have a trusted confidante to advise or guide them. The question is, what will those customers do? Will they go to the trouble of seeking out someone at your bank? Or will a better advertised rate or a recommendation from a friend drive them to a new bank?

Knowing what you know about your market, you can probably guess how they'll respond. And if you don't like the answer, it's probably time to get out there and meet your customers.

Survey Methods

Results are based on a Gallup Panel study and are based on mail and web surveys completed by 42,85 national adults, aged 18 and older, conducted 8/13-9/23/2008. Gallup Panel members are recruited through random selection methods. The panel is weighted so that it is demographically representative of the U.S. adult population. For results based on this sample, one can say with 95% confidence that the maximum margin of sampling error is ±1 percentage points. Margins of sampling errors vary for individual subsamples. In addition to sampling error, question wording and practical difficulties in conducting surveys can introduce error or bias into the findings of public opinion polls.