Companies around the globe have been investing in the development of new channels of customer contact. Most often, these channels have used technology to replace direct person-to-person contact.

|

Technology seems to offer a win-win solution. Companies have been confronted with a mandate to improve efficiency and reduce costs while also meeting the information-seeking and transactional requirements of their increasingly time-starved customer base. Customers have been seeking speedier and more convenient access, wherever and whenever they might feel the need. Technology promises to address the needs of company and customer, improving transaction efficiency while providing the sorts of additional customer benefits that lead to increased engagement. (See graphic "How Engaged Are Your Customers?")

So retailers have created online shopper Web sites, airlines have established mobile phone update links, and hotels have established online reservation services. All provide customers with attractive options: They no longer need to drive to the bookstore, the grocery, or the video rental store, then wait in long lines to get what they want. They no longer have to wait on hold, hoping that a reservations or customer service agent will finally take their phone call. Instead, they can perform these tasks online -- and at 2:00 a.m. if that's their desire.

|

Banks have been particularly active in this area, responding to customers' desires for increased access to information and to their money. ATMs have long been ubiquitous, allowing customers to deposit and withdraw cash around the clock. In many countries, customers can open new accounts, transfer funds, check balances, and pay their bills online, without ever stepping foot in a bank. More recently, banks have been offering the ability to conduct routine transactions through the use of a wireless device or mobile phone. Digital touchpoint options are everywhere.

What could be simpler? And could there possibly be anything wrong with this picture?

Transactions versus relationships

Well, there's a critical issue here, and it's one that should concern every retailer, whether bookstore or bank. Companies ultimately succeed based on their ability to build customer relationships, not just speedy process transactions. (See "The Engagement Imperative" and "Managing the Value of Your Brand" in the "See Also" area on this page.)

And the situation gets more complicated. Speed and access are often key customer needs -- and fundamental expectations. But the tools that promise speed and access are now the basic "table stakes" necessary for any airline, video renter, or bank to compete in the markets in which they operate. In the United States, for example, Wells Fargo Bank offers online banking. But so do Wachovia, Bank of America, HSBC, Citibank, and any number of others.

It's crucial for a bank to have a Web site. It's also crucial for a bank to have ATMs, checking accounts, and computers that keep accurate records. But every bank can claim to meet these basic service requirements. What banks really need is some way to show prospects and customers that they are different from their competitors. Differentiation is essential for marketers seeking to establish an enduring bond with their customers.

And here lies the dilemma. The factors that have typically had the greatest impact on customer engagement -- and that have offered service marketers (including banks) the greatest opportunities to exceed customer expectations and differentiate the customer experience -- are the "people" factors. (See "People Who Need People" in the "See Also" area on this page.) But these human interaction opportunities are the ones that are being reduced or, in some cases, eliminated.

Does this mean that many companies are headed down the slippery slope to becoming commodities -- and that customer engagement is well on its way to becoming an endangered species? Hardly. What it does mean, however, is that today's marketers have to pay close attention to all the opportunities that lie before them -- seeing each as a chance not merely to process transactions and fulfill requests, but to foster connected, engaged customer relationships.

Consider the case of the "people" component. A personal, face-to-face encounter with an employee is no guarantee that the experience will prove to be engaging for the customer. Some employees are able to create customers for life. But some breed angry, disconnected customers who are anxious never to repeat the experience. "People" are a channel of customer contact, and that contact can be engaging -- or disengaging.

Consider also the case of the call center, another channel of contact used by a great many companies to expand their reach and hours of availability. Some telephone interactions contribute to a lasting relationship. But the telephone doesn't ensure that interactions enhance engagement. Far too many "conversations" begin with a seemingly interminable time on hold listening to recorded messages, after which the customer is finally routed to an outsourced provider with neither the ability nor the inclination to solve the customer's problem. Telephones represent a channel of contact; they don't guarantee that this contact will help build a bond.

|

It's not the existence of the tool that matters. It's the quality of the experience that results from how the tool is designed, orchestrated, and managed.

Engaging in a digital world

A recent Gallup study of banking customers, sponsored by Adobe Systems, underscores the opportunity as well as the challenge facing today's marketers. The study involved a survey of more than 2,100 retail banking customers in Japan, France, Germany, the United Kingdom, Canada, and the United States. The data attest to the rise in banking customers' use of the new digital touchpoints. For example, in the United Kingdom, France, Canada, and the United States, more than half of all customers reported using their bank's Web sites, and about 1 in 10 used some form of mobile device to conduct banking transactions.

Has the growth of digital touchpoints, projected by Forrester Research to continue its so-far dramatic expansion, enhanced customer relationships -- or has it weakened them? The answer, this Gallup study reveals, is neither.

Very much like the "people" or the "telephone," the availability of interactive technologies such as Web sites or mobile service by itself ensures nothing. In this study, whether or not a retail banking customer used his bank's Web site made no difference to his level of engagement. What did make a big difference was the nature of the interaction that the bank's Web site offered -- and how that interaction made the customer feel.

Not all people are engagement builders. Not all phone call experiences make for stronger relationships. And not all Web sites are created equal. While some Web sites may be a pleasure to navigate, others are a nightmare. While some offer clear and useful features, others are an annoying excursion into a world of redundant questions, hidden pathways, and confusing options.

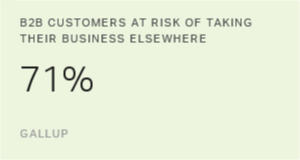

Well-designed and user-friendly points of contact help build engagement. Our survey found that more than 7 in 10 customers (71%) who were extremely satisfied with their bank's Web site expressed a strong sense of engagement (were "engaged" or "fully engaged") with their bank. In clear contrast, only about 1 in 4 Web site users (27%) who were anything less than extremely satisfied with that experience indicated a sense of engagement. That's actually a bit lower than the engagement levels noted for those who don't use their bank's Web site at all (32%).

What we've found is that an engaging digital experience can meaningfully support engagement to the bank that provides that experience. However, anything less than a highly satisfying Web site experience generates customer disengagement. Engagement isn't built by experiences that are merely OK.

This point is reinforced in an April Advertising Age discussion of the impact of micro-interactions. David Armano notes that "Micro-interactions are the everyday exchanges that we have with a product, brand and service. Each one, in and of itself, seems insignificant. But combined they define how we feel about a product, brand or service at a gut emotional level." Little things mean a lot. (See "Brand Interactions Are the Future" in the "See Also" area on this page.)

The challenge for organizations is to create experiences that will seamlessly support an engaged customer relationship. That's the assignment Adobe Systems is helping its own customers achieve, having recognized that engaged customers are not just "nice to have" or "great to think about." Rather, engagement represents what Adobe has termed a new business mandate -- one that challenges technology just as it challenges everyone who, on behalf of a company, comes in contact with a customer.

"Our customers are at the leading edge of the engagement challenge," said Doug Mack, vice president and general manager of hosted and consumer solutions for Adobe. "The effective implementation of technology is one of the best ways for companies to cultivate more engaged customers and attain a competitive edge. However, the market never stands still, which makes engagement a constant work in progress."