Story Highlights

- Baby boomers vary more than stereotypes suggest

- There are really two cohorts of boomers

- Older boomers are spending more on discretionary items than a year ago

This article is part of an ongoing series analyzing how baby boomers -- those born from 1946-1964 in the U.S. -- behave differently from other generations as consumers and in the workplace. The series also explores how the aging of the baby-boom generation will affect politics and well-being.

Baby boomers are often portrayed in the popular press as a monolithic group of individuals who behave in roughly the same ways and possess the same attitudes. But do these observations hold for all boomers? Or are they emblematic of just some?

Recent Gallup analysis of boomers' personal spending patterns suggests that these patterns vary more than stereotypes suggest. These differences matter most to marketers who hope that boomers are finally re-opening their wallets after the global financial crisis and will spend some of their discretionary income with their companies.

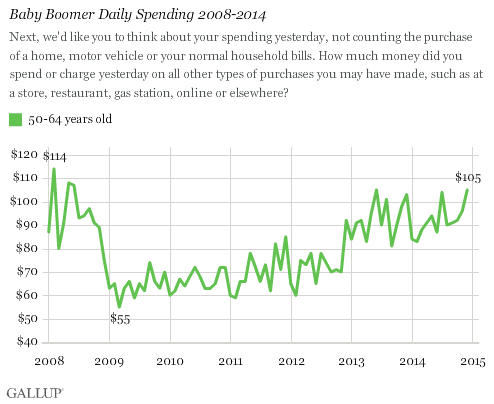

The global financial crisis hit baby boomers particularly hard. According to Gallup Daily tracking research, self-reported daily spending among Americans aged 50 to 64 years old (roughly the ages of the baby boomer cohort) reached a low of $55 in March 2009. About one year earlier (February 2008), daily spending in this group had been at $114. By last December, this cohort's daily spending had rebounded to a five-year high of $105 per day. Nonetheless, the trend suggests that the daily spending among boomers has been increasing since bottoming out in 2009. But exactly what are they spending more on?

Gallup research conducted last spring revealed that while 45% of U.S. consumers reported that they were spending more than a year ago, their increased spending was on household essentials, including groceries, gasoline, utilities and healthcare rather than on discretionary purchases such as travel, dining out, leisure activities, consumer electronics and clothing. About four in 10 baby boomers (44%) in that same study reported that they were spending more than a year ago, and their increased spending followed the same pattern -- more on things they need, not on things they want.

According to demographers, there are really two different cohorts of baby boomers. "Leading-edge" boomers were born between 1946 and 1955 and came of age during the tumultuous Vietnam War and Civil Rights eras. "Trailing-edge" boomers were born between 1956 and 1964 and came of age after Vietnam and the Watergate scandal.

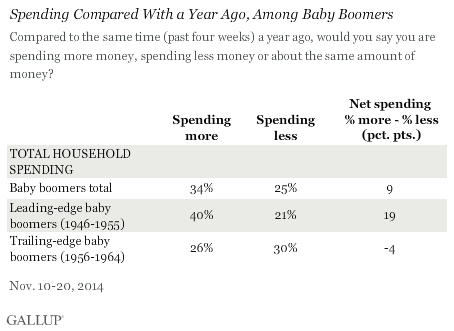

Leading-Edge Boomers Spend More Than Trailing-Edge Boomers

In general, a higher proportion of leading-edge baby boomers report that they are spending more today than a year ago compared with trailing-edge boomers. Net spending change -- defined as the percentage of consumers indicating that they are spending more today than a year ago minus the percentage saying they are spending less -- is positive for leading-edge boomers but negative for trailing-edge boomers. This 23-percentage-point gap between the cohorts means that more leading-edge (older) boomers are spending more overall and more trailing-edge (younger) boomers are spending less.

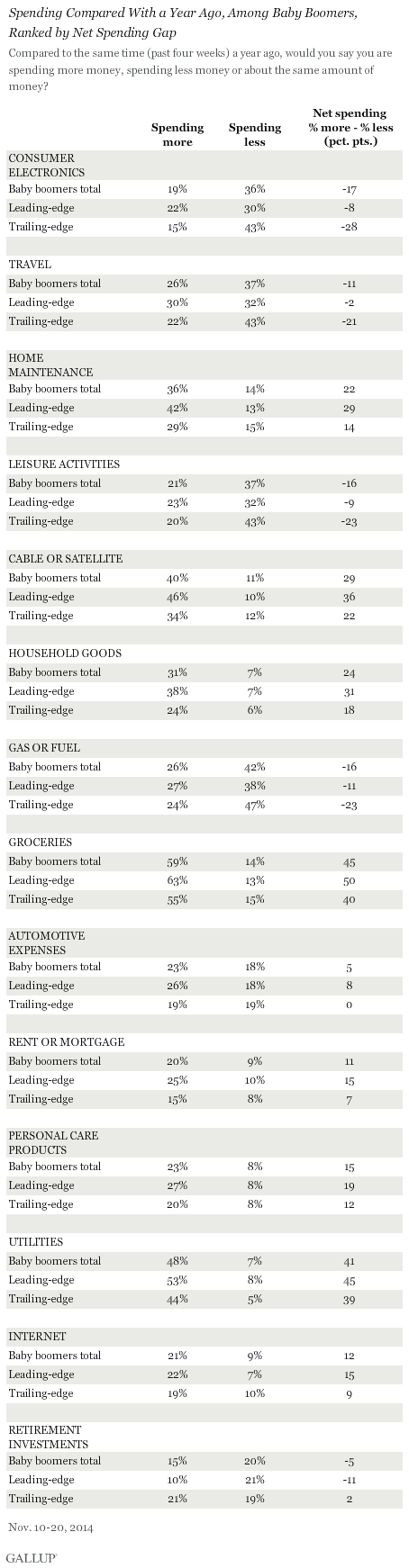

But exactly what are leading-edge boomers spending relatively more on than trailing-edge boomers? When we take a deeper look at self-reported spending changes in a number of categories, we find that leading-edge boomers report spending more today than a year ago across the board, even though Gallup's Daily tracking spending data show the two boomer cohorts spending roughly the same daily amount ($99 versus $100 per day for the most recent reporting period, respectively). The lone exception is retirement investments, where more than twice as many trailing-edge boomers report spending more today than a year ago as leading-edge boomers do.

Discretionary spending categories -- leisure activities, consumer electronics and travel -- all show negative net spending changes, indicating that more baby boomers feel they are spending less today compared with a year ago on these categories rather than spending more. In contrast, nondiscretionary spending categories -- such as groceries, automotive expenses, rent or mortgage and utilities -- all show positive net spending changes, indicating that more baby boomers feel they are spending more today compared with a year ago on these categories rather than spending less. The exception to this pattern is gas or fuel, which has seen unprecedented declines in prices over the last few months.

But beneath these more general differences in spending, net spending for leading-edge boomers is much larger for nondiscretionary purchases than trailing-edge boomers. In other words, leading-edge boomers are spending more today than a year ago on nondiscretionary purchases than trailing-edge boomers.

Substantial Differences in Spending by Different Segments

Gallup's analysis suggests that there are substantial differences in the fiscal experiences of different segments of baby boomers. Leading-edge boomers (aged 59 to 68) may no longer be burdened with some significant financial responsibilities, such as college tuition, mortgages, children's expenses and investments, while trailing-edge boomers (aged 50 to 58) still are. As a result, leading-edge boomers report spending more in the past year in all categories except investments, particularly in the discretionary spending categories of travel, consumer electronics and leisure activities.

The takeaway for marketers here is pretty clear, and it should come as welcome news to many: Leading-edge boomers appear to have greater latitude in their spending -- and are applying it to things they would prefer to do rather than things they have to do. For companies hoping to market to baby boomers, now is the time to begin to think of these two very different cohorts as distinct groups, with very different needs and responsibilities, and market to them accordingly. Older boomers, free of family financial obligations and focusing on new possibilities, will likely respond in ways that younger boomers won't -- or simply can't for now.

Survey Methods

Results for this Gallup poll are based on telephone interviews conducted Nov. 10-20, 2014, on the Gallup U.S. Daily survey, with a random sample of 1,539 adults, aged 18 and older, living in all 50 U.S. states and the District of Columbia. For results based on the total sample of national adults, the margin of sampling error is ±3 percentage points at the 95% confidence level.

Each sample of national adults includes a minimum quota of 50% cellphone respondents and 50% landline respondents, with additional minimum quotas by time zone within region. Landline and cellular telephone numbers are selected using random-digit-dial methods.

Learn more about how the Gallup U.S. Daily works.