This post is part of Gallup's ongoing series on the shifting landscape for financial institutions. It provides insights into channel optimization, emerging customer behaviors and preferences, product penetration and relationship growth, engaging the most critical affluent and business customers, and reshaping banks' overall value proposition.

When free checking took over the banking industry, differentiating on customer service or the "customer experience" came into much greater focus. Products had become largely commoditized, and banks were anxious to grow their deposits, which generated significant fee revenue and capital for lending. Through superior customer service, the thinking went, banks could attract those deposits and grow their bottom line. And for many banks, this was a highly successful strategy.

The Great Recession and financial crisis ushered in a host of new regulations, scrutiny, and economic realities, sounding the death knell for most "free" products and generally focusing banks more keenly than ever on all things sales-related -- cross selling, up-selling, acquisition, etc. Indeed, much of our consulting with banking clients these days is focused on how they can improve and expand the "needs-based" conversations they have with clients. While no one is denying the importance of sales, the customer experience remains critically important in driving both near-term profitability and healthy long-term customer relationships. In fact, most banks' service programs (if designed and executed well) will pay for themselves many times over in terms of increased engagement with the bank.

Let's look at three tangible benefits banks derive from their fully engaged customers (attitudinally loyal and emotionally attached to the bank) compared with their actively disengaged customers (lacking any kind of strong connection).

1. Increased Revenue, Wallet Share, and Product Penetration

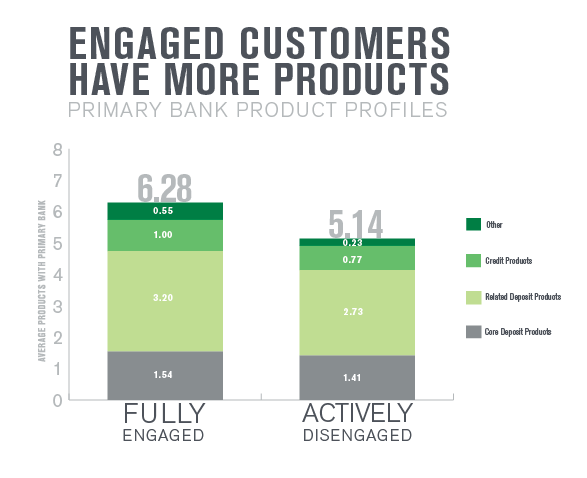

According to Gallup's latest U.S. Retail Banking study conducted in November 2013, customers who are fully engaged bring $402 in additional revenue per year* to their primary bank compared with those who are actively disengaged. This rockets up to $869 in additional revenue for mass affluent clients (those with $100K to $1M in investable assets). Take a minute and multiply these numbers by the size of your bank's customer base, and you will usually find that the financial benefit of fully engaging your customers far outweighs the cost of the surveys, training, and incentives for running a solid customer experience program. Imagine what could happen if you fully engaged all of your customers!

This additional revenue is coming from several sources. Fully engaged customers have 10% greater wallet share in deposit balances with their primary bank, and 14% greater wallet share in investments. Across a broad array of product categories in four general buckets -- deposit accounts, deposit-related "add-ons," credit products, and fee-based or advisory products (investments, insurance, financial advice) -- fully engaged customers average 1.14 additional product categories with their primary bank than do customers who are actively disengaged. As you might expect, these differences are most pronounced in the more discretionary (and potentially lucrative) categories. For example, fully engaged customers have more than twice the number of investment, insurance, or advisory products with their primary bank than do their actively disengaged counterparts.

2. Greater Purchase Intent and Consideration

It's not just the current state of the relationship that benefits from customer engagement. Banks can also rely more assuredly on fully engaged customers to consider their bank for future needs and to grow their overall relationship. From our research, fully engaged customers are far more likely to report a strong intent to purchase from their primary bank over the course of the next year. This runs the gamut from simply adding a service that supports an existing product to satisfying higher level needs, such as opening investment accounts or seeking financial advice. Even if these intentions don't materialize into immediate sales, when you fully engage your customers you have overcome at least one great obstacle to selling more -- being in their consideration set. This can be especially important for retail-focused banks that may be looking to expand their reach into more complex and lucrative product and service categories.

3. Fostering a Life-Long Relationship

And finally, if the current financials or future considerations don't sway you, how about some compelling data that shed light on just how much of a role banks can play in their customers' lives when those customers are fully engaged with their bank: More than half (54%) of fully engaged customers strongly agree that their bank helps them make their financial dreams come true, and a similar percentage (55%) say that their primary bank helps them get more enjoyment out of life. You certainly don't hear that sentiment expressed very often when the subject turns to banking. And, perhaps most importantly for bankers who are in it for the long haul, nearly three-quarters (71%) of fully engaged customers believe that they will use their primary bank for the rest of their life. Finance is indeed personal. When you are able to fully engage customers, you can also play an important role in enriching their lives.

*Modeled on deposit and investment balances, fees, card balances and usage, and loans with primary bank.