This post is part of Gallup's ongoing series on the shifting landscape for financial institutions. It provides insights into channel optimization, emerging customer behaviors and preferences, product penetration and relationship growth, engaging the most critical affluent and business customers, and reshaping banks' overall value proposition.

SERVICES

In banking, we often hold these "truths" to be self-evident: Large banks offer their customers a wide array of products and services including leading and varied technology, but they don't care as much about their customers. Here's another: Smaller banks offer their customers a high level of personal service built around an amazing customer experience, but often lack technology. However, according to Gallup research on retail banking brand attributes, while some of these long-held beliefs are true, others need to be revisited.

Myth: Large Banks Don't Care as Much as Small Banks

While it is true that national banks score better or as well as their smaller counterparts on attributes like, "Lets me bank anywhere, anytime, anyway I want," and "Rewards me for the relationship I have with them," they also do just as well or slightly better than their smaller counterparts when it comes to helping their customers think about and manage their finances to meet their goals. This should really come as no surprise, as these are the banks that have the most robust investment services spanning affluence groups and solid web-based solutions for financial planning.

Large banks also tend to better train their platform employees on how to have a sales conversation that actually spans the larger pictures of a customer's life rather than just asking basic questions like how many checks they write a month and if they want to use mobile banking. When it comes to caring about customers' long-term financial goals, this manifests with customers saying these large banks do just as well as their smaller counterparts on attributes like, "Leads you down a path to your financial goals." So, while maybe not known for their warm and fuzzy attitudes, national banks have proven that they do care about their customers' financial futures just as much as their smaller colleagues.

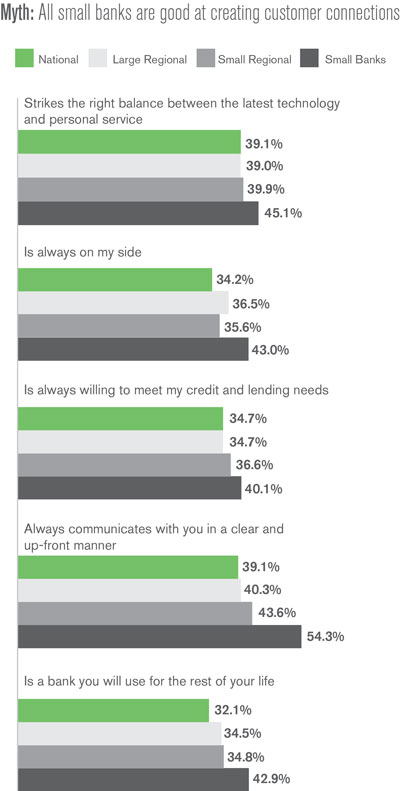

Myth: All Small Banks Are Good at Creating Customer Connections

Yes, in general, the smallest of the small banks are good at creating personal connections and being there for their customers in the way that the largest banks are not. But not all smaller banks are created equal. Small regional banks do not score that much better than their large regional and national counterparts and actually score worse than other smaller banks when it comes to attributes like, "Strikes the right balance between the latest technology and personal service," "Is always on my side," and "Is a bank you will use for the rest of your life." This begs the questions - what do these small regional banks stand for? What is their value proposition? If customers aren't getting better technology, better financial planning, or better service, how will they compete in the future?

We may still live in a time when a lot of customers pick a bank because the branch is closer to their house or their parents set up an account for them when they were kids, but as technology changes, including how we interact with banks, these reasons are becoming less important. Smaller regional banks will need to either invest more in the people side of the business or the technology side of the business to have a chance at creating a compelling differentiation in the market.

National: 5000+ branches or $400B+ deposits

Large Regional: <$400B to >$100B in deposits, 1000 to <5000 branches

Small Regional: 400 to <1000 branches & $50B to <$100B in deposits

Small Banks: <400 branches or <$50B in deposits (does not include Credit Unions)