This post is part of Gallup's ongoing series on the shifting landscape for financial institutions. It provides insights into channel optimization, emerging customer behaviors and preferences, product penetration and relationship growth, engaging the most critical affluent and business customers, and reshaping banks' overall value proposition.

I have two banks. When I call the 800 number of Bank A, I somehow always end up purchasing or using additional products and services, even though I didn't call with the intention of doing either. However, when I call Bank B, I end up annoyed and spend several minutes daydreaming about cutting my ties to it entirely. I would really like to say something along the lines of, "I have issues, I am NOT calling you just to chat, and you are wasting your time trying to sell me something unrelated to my issue that I don't need. How can you do that to me? Can't you tell I'm already annoyed and busy? And asking if you can sell me something before launching into your pitch isn't helping."

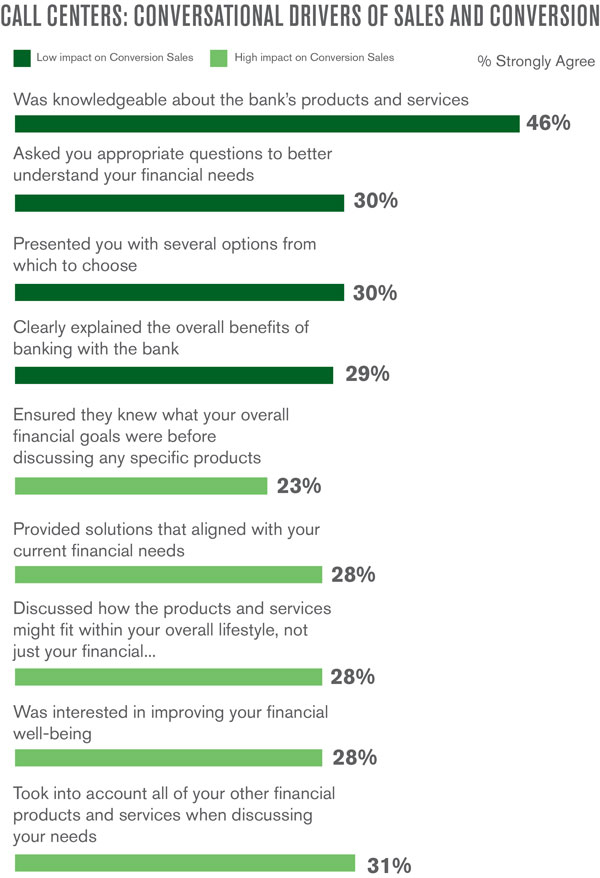

My experiences at Bank A and Bank B are similar to what Gallup has found to be true for all consumers. In our retail banking research, we have discovered that call center employees successfully drive sales and conversion when they use tactics that are -- not surprisingly -- all about the customer and not about the bank. But most banks are failing to get it right.

Let's use an example: I was going on an international trip and in the frenzy of getting ready, I nearly forgot to call my banks to activate my debit cards for international usage. I called Bank B and explained what I needed to the representative and, in the course of our conversation, it naturally came up that I was leaving in an hour. There was silence on the other end as she was clicking on the keyboard to set up my debit card. Fail No. 1 -- the representative couldn't multitask and missed making a connection with me through small talk. When she was done, she then asked if she could tell me about solutions that could meet my needs. Fail No. 2 -- this obviously wasn't the time to do this, but she had to check her script compliance box. When I said, "No, I don't have the time," she told me I could call back anytime because they have some personal and auto loan offers that may be right for me. Fail No. 3 -- at no point did we ever discuss nor should she ever have been able to deduce from our conversation that I, in any way, needed a loan. She wasted my time and annoyed me by pitching an unneeded product.

Would I "strongly agree" that this representative was knowledgeable about the bank's products and services, and that she asked me questions to understand my needs? Sure. On the other hand, I would "strongly disagree" with any of the attributes that actually drive conversion, because she seemed to miss the point of our entire conversation.

Contrast this with Bank A, where the woman I spoke to practically squealed with excitement when I told her where I was going and then proceeded to ask me all sorts of questions about my trip while she made the necessary changes to my account. She ended with, "I know you are in a hurry but I just wanted to make sure you know you get x, y, and z benefits when you are traveling abroad with us." I had no idea, and I hadn't looked into it because I wasn't intending to actually use Bank A while I was abroad, it was just my backup. She then proceeded to tell me how those benefits would match up to things I had mentioned I was going to do on my trip, and how I would save money in the process.

Without a doubt I would strongly agree that Bank A's representative provided solutions to meet my current financial needs, looked out for my financial well-being, and took into account my lifestyle when discussing my needs. In the end, I used Bank A's products more than any other financial product at my disposal while on vacation, and I'm sure they made a pretty penny off all the fees I generated for them. By looking out for me and customizing the conversation to me and my needs, both Bank A and I won.

If I had written this blog six months ago, I would have titled "Bank A" as "Bank B," because I did not consider it to be my primary bank. I didn't have a reason to go into the branch and its mobile and online banking were on par with my other bank. This emotional and financial primary bank switch was driven by my call center interactions. While logically I know that in both cases I am contacting a massive call center with people in cubicles wearing headsets looking up information about me on computers, Bank A's employees seem to "get me." They are nice, they read my verbal cues well, and seem genuinely interested in me and my well-being. In short, they put me, not the bank, first. I will continue to call Bank A, I will continue to put more money in my accounts there, and I will continue to strongly consider it for all my future financial needs. Because, like all customers, when properly engaged and sold to, I reward companies with my loyalty and my business.