This post is part of Gallup's ongoing series on the shifting landscape for financial institutions. It provides insights into channel optimization, emerging customer behaviors and preferences, product penetration and relationship growth, engaging the most critical affluent and business customers, and reshaping banks' overall value proposition.

We recently shared a framework we developed to help banks turn everyday transactions into sales conversations. The framework, which moves from conversational foundations and basic assistance to a more holistic focus and an overall financial vision, can be implemented for all key customer-facing roles (tellers, bankers, contact center agents, relationship managers, etc.) across a variety of product types and customer segments. Each specific conversation and situation dictates how far up the framework a bank associate should proceed with a customer. Not every conversation should involve an in-depth discussion of the customer's financial future, but ideally all relationships should get to that point over time.

Of course, we know that consulting is littered with well-intentioned frameworks that fail to make a real-world impact on their intended audiences, and they fail for a variety of reasons. One reason, unfortunately, is that frameworks can be highly logical and appealing in the conceptual world only, and don't translate very well to real-world situations. That isn't the case here. When we tested this conversational framework in one of our recent retail banking industry studies, we found strong evidence that these key conversational elements lead to two important outcomes: 1) a highly satisfying customer experience, and 2) increased sales.

When implementing a sales program with our banking clients, the hierarchical nature of the framework tends to remain quite constant -- even though the specific elements at each level of the framework are customized to fit the client's unique situation. While some customers in some situations require very little from the banker to open an account -- the quintessential "low-hanging fruit" -- banks (and customers) will see significant benefits when the conversation is elevated to the higher levels of the framework.

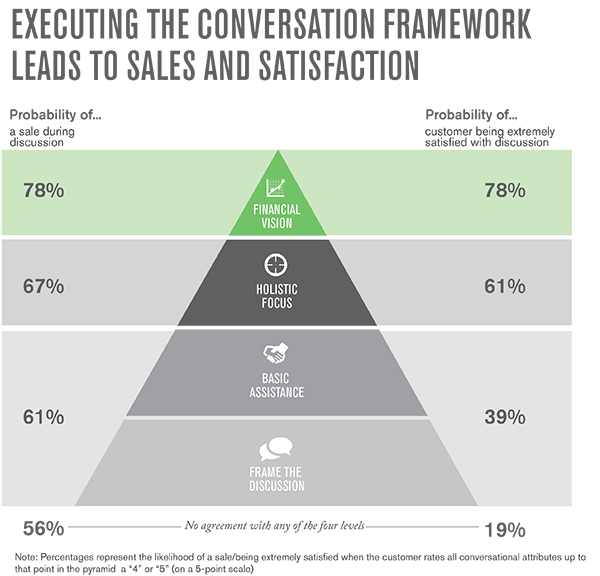

Low-Hanging Fruit: Even when bankers don't perform any of the conversational elements particularly well (scoring a 3 or less on a 5-point scale), slightly more than half of banking customers still tell us that they opened an account, purchased a product, or added a service during that visit. In other words, these customers represent the classic low-hanging fruit -- customers who come into the branch (for example) with the express purpose of obtaining some kind of product. These customers typically don't require a terribly in-depth or even well-executed conversation with their banker. What we do notice, however, is that despite purchasing something that day, they aren't very satisfied with the experience -- only 19% rate it a "5" on a 5-point scale. It's quite likely that these bankers left something on the table that day in terms of additional sales and hurt their chances for future sales.

Solid Foundation: If bankers are able to build a solid foundation during the conversation, they see immediate dividends. When customers rate foundational elements highly -- bankers properly frame the discussion, ask appropriate questions, and dispense useful advice -- we find a noticeable increase in the likelihood of sales (from 56% to 61%) and in customers being extremely satisfied with the interaction (from 19% to 39%).

Pyramid Power: The better the banker is able to execute on the more complex, holistic, and visioning elements -- the higher levels of the conversational pyramid -- the more likely they are to garner a sale during that conversation. And the payoff is greater at each successive level of the pyramid. While the likelihood of a sale increases more modestly from 56% when none of the elements are done well to 61% when only the basics are executed, that likelihood increases to 67% when the conversation is also holistic in nature, and further to 78% when the conversation includes financial vision (e.g., educating the customer on their financial potential or how their needs may change over time). So, while not every sales conversation will (or should) reach the financial vision pinnacle, it remains a worthwhile -- and bottom-line focused -- goal for all relationships.

Shared Success: While banks (with good reason) are drawn to the sales impact presented here, it is important to note that when a banker executes all elements of this framework successfully, both sales and customer satisfaction are maximized. Not only can the bank and the banker feel good about delivering more sales for their organization, they can also feel good that they are delivering a more positive experience for the customer, which can be an important element of the organization's overall mission and branding. Associates can talk about "meeting customer needs" and delivering an "exceptional customer experience" as opposed to the more sterile, internally-focused "selling more." Of course, if a customer is more satisfied with their conversational experience, they will also be more likely to consider that bank and that banker the next time they need a financial product.