Story Highlights

- Half of nonretirees expect 401(k) to be a major income source in retirement

- This is up from a low of 42% in April 2009, but still below earlier highs

- Planned reliance on Social Security is near 17-year high

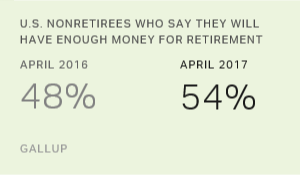

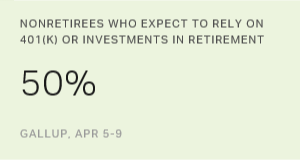

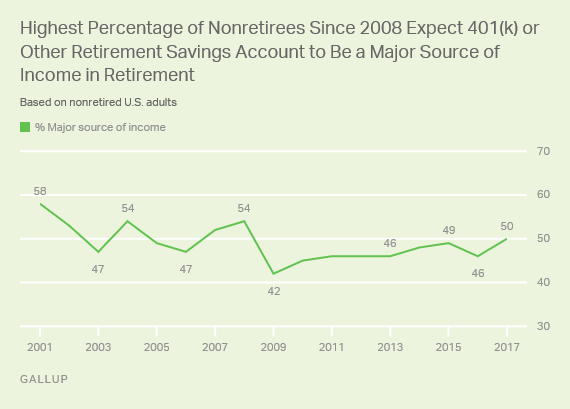

WASHINGTON, D.C. -- With the stock market hovering near historical highs a full eight years into the bull market, 50% of nonretired Americans expect their 401(k) or other retirement savings account to be a major source of income in their golden years. This expectation is the highest (by one point) that Gallup has recorded since April 2008, just before the Wall Street financial crises sucked more than $2 trillion out of U.S. retirement accounts.

While improved, nonretirees' expectation that their retirement account will significantly fund their post-working years has not returned to where it was prior to the financial crises. The percentage expecting their 401(k), IRA, Keogh or other retirement account to be a major income source averaged about 52% in Gallup polling each April from 2001 through 2008. The highest point for this outlook was 58% in 2001, at the tail end of the dot-com boom.

Relatedly, Gallup finds fewer Americans owning stocks than in the past. Prior to the 2007-2009 recession, at least 60% of U.S. adults said they had money invested in stocks or in a mutual fund, 401(k) or IRA. But this began sliding in 2009, falling to 52% by 2013, and is at 54% today.

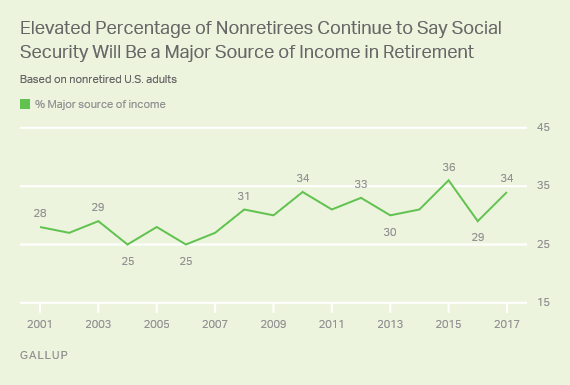

At the same time, the 34% of nonretirees counting on Social Security as a major source of retirement income is near its peak in Gallup's 17-year trend. Prior to the recession, between 25% and 29% thought they would rely this heavily on Social Security, but this increased to 31% during the recession and has since ranged from 29% to 36%.

One in Four Counting on Savings Accounts, Pensions for Retirement

Retirement savings accounts and Social Security are the top two sources of income that today's nonretirees expect to rely on the most. This is true not only in the percentages predicting each will be a major source of income in later years, but also in terms of the combined percentages saying each will be a major or minor source -- roughly 80% for both.

| Major source | Minor source | Not a source | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| % | % | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| A 401(k), IRA, Keogh or other retirement savings account | 50 | 30 | 18 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Social Security | 34 | 45 | 19 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other savings such as a regular savings account or CDs | 25 | 43 | 31 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| A work-sponsored pension plan | 25 | 29 | 44 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| The equity you have built up in your home | 21 | 42 | 35 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Part-time work | 19 | 52 | 27 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Individual stock or stock mutual fund investments | 18 | 37 | 43 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Annuities or insurance plans | 9 | 34 | 55 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Rent and royalties | 9 | 26 | 63 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Money from an inheritance | 6 | 28 | 64 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Gallup, April 5-9, 2017 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Following these workhorses of retirement security, regular savings accounts or CDs, as well as work-sponsored pension plans, figure as major potential income sources for 25% of nonretirees. More than half of nonretirees are counting on each as at least a minor source of income.

Next up are home equity, part-time work and individual stock or stock mutual fund investments. Roughly one in five nonretirees predicts each of these will be a major income source for them, and majorities of 55% to 71% identify each as at least a minor source.

Fewer than one in 10 nonretirees believe annuities or insurance plans, rent or royalty income, or inheritance money will be a major income source for them in retirement. In addition, less than half expect these to be either a major or minor source.

More Eyeing Savings Accounts, Part-Time Work for Retirement Income

The current rank order of expected retirement sources is similar to what Gallup's annual Economy and Personal Finance survey has found each year since annual tracking of this measure began in 2001. The 2017 installment was fielded April 5-9.

Nonretirees' current views are similar to those recorded last year. But compared with the baseline measure in 2001, more now predict that traditional savings accounts, part-time work and Social Security will be significant income streams in their retirement. The biggest declines are for work-sponsored pensions and 401(k) and other retirement accounts, as well as individual stock investments.

Expectations for relying on rent or royalties, annuities or insurance plans, inheritance money and home equity are fairly stable.

| 2001 | 2017 | Change | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| % | % | pct. pts. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other savings such as a regular savings account or CDs | 16 | 25 | +9 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Part-time work | 10 | 19 | +9 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Social Security | 28 | 34 | +6 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Rent and royalties | 5 | 9 | +4 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Annuities or insurance plans | 7 | 9 | +2 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Money from an inheritance | 7 | 6 | -1 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| The equity you have built up in your home | 24^ | 21 | -3 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Individual stock or stock mutual fund investments | 24 | 18 | -6 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| A 401(k), IRA, Keogh or other retirement savings account | 58 | 50 | -8 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| A work-sponsored pension plan | 34 | 25 | -9 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| ^ Based on 2002 poll | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Gallup | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Current Retirees Mainly Depend on Social Security, Followed by Pensions

In addition to asking nonretirees about the sources of income they anticipate relying on when they retire, the survey also asks those who have already retired what they are actually using.

Current retirees report depending the most on Social Security, with 55% calling it a major income source for them today and 89% saying it is either a major or minor source. This is followed by a work-sponsored pension, with 38% calling it a major source, and retirement savings accounts such as a 401(k) or Keogh, at 24%.

| Major source | Minor source | Not a source | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| % | % | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Social Security | 55 | 34 | 10 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| A work-sponsored pension plan | 38 | 20 | 40 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| A 401(k), IRA, Keogh or other retirement savings account | 24 | 35 | 38 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| The equity you have built up in your home | 20 | 28 | 48 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Individual stock or stock mutual fund investments | 18 | 31 | 49 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other savings such as a regular savings account or CDs | 12 | 38 | 48 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Annuities or insurance plans | 7 | 26 | 62 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Rent and royalties | 5 | 18 | 75 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Money from an inheritance | 5 | 11 | 82 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Part-time work | 5 | 20 | 74 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Gallup, April 5-9, 2017 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

There has been little variation since 2001 in retirees' reports of their actual reliance on various income sources.

Bottom Line

Most future retirees expect to depend on mainly Social Security or their 401(k) or other retirement investment account in their retirement. Just after the Great Recession, fewer retirees were sure their personal investments would do the job, leaving more Americans to say they would likely depend on Social Security.

Today, confidence in retirement investments is about halfway restored to where it was prior to the recession, which is likely a positive reaction to the strong stock market. This is also seen in surging investor confidence in the investing climate, as measured by the Wells Fargo/Gallup Investor and Retirement Optimism Index. However, nonretirees' expectation for relying on Social Security has not waned accordingly. Rather, slightly more plan to lean heavily on both income streams, perhaps as pensions disappear.

These findings underscore how important it is that legislative and financial policymakers do their jobs well. That means helping to spur the economic growth needed to support both a strong stock market and thriving labor market. The latter alone could go a long way in improving the Social Security system's fragile balance sheet. However, to the extent that policy changes are needed to keep the Social Security trust fund solvent, leaders and the public must be willing to make some tough choices. Future retirees are counting on it.

Historical data are available in Gallup Analytics.

Survey Methods

Results for this Gallup poll are based on telephone interviews conducted April 5-9, 2017, with a random sample of 1,019 adults, aged 18 and older, living in all 50 U.S. states and the District of Columbia. For results based on the total sample of national adults, the margin of sampling error is ±4 percentage points at the 95% confidence level. For results based on the sample of 718 nonretirees, the margin of sampling error is ±5 percentage points. For results based on the sample of 301 retirees, the margin of sampling error is ±7 percentage points.

All reported margins of sampling error include computed design effects for weighting.

Each sample of national adults includes a minimum quota of 70% cellphone respondents and 30% landline respondents, with additional minimum quotas by time zone within region. Landline and cellular telephone numbers are selected using random-digit-dial methods.

View survey methodology, complete question responses and trends.

Learn more about how the Gallup Poll Social Series works.