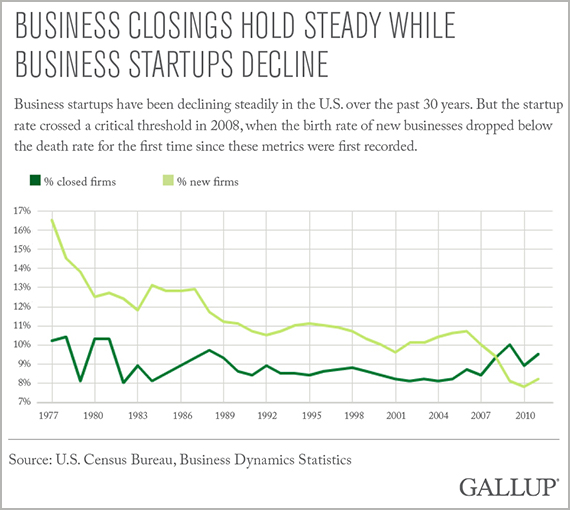

Business startups have been declining steadily in the U.S. over the past 30 years. In 1977, 16.5% of businesses in America were less than one year old, according to data from the U.S. Census Bureau. By 2011, that figure had dropped by half, to just 8.2%. The percentage of businesses that closed each year remained relatively constant over the same time frame, at about 9%.

But in 2008, the startup rate crossed a critical threshold. The percentage of new businesses created that year was smaller than the percentage of businesses that closed down. In other words, the birth rate of new businesses dropped below the death rate for the first time since these metrics were first recorded -- and that downward track has continued.

Gallup pointed out this decline earlier in the year, and the recent publication of a summary paper by two researchers at the Brookings Institution sparked another round of media attention. Despite all this research, there has been no definitive answer as to why the rate of U.S. startups has declined so precipitously.

New Gallup research into the drivers of entrepreneurship at the individual and national levels offers an explanation of this sharp decline. Recent Gallup research suggests that a crucial factor influencing the declining rate of U.S. startups is a decline in the personal savings rate.

Securing adequate financing is a challenge for business owners and entrepreneurs -- and that financing comes predominantly from personal savings, Gallup research shows. These findings are similar to those shown in research by the Kaufmann Foundation on business owners and startups.

- The Wells Fargo/Gallup Small Business Index has consistently found that small-business owners depend most on personal savings for startup funding. When Gallup first asked entrepreneurs about their sources of startup funding in 2006, 73% of small-business owners mentioned personal savings as a source, while 37% cited a loan or line of credit as the next most common source. When Gallup asked this question in 2014, 77% cited personal savings as a source of startup funding, followed again by a loan or line of credit (41%) as the next most common source.

- The Sam's Club/Gallup Microbusiness Tracker also shows that 60% of microbusiness owners -- those who own businesses with five or fewer employees, including themselves -- depended on personal savings to finance their business. This is particularly true of those who have started their business: 79% of those who started their microbusiness in the past year had drawn on their personal savings for financing compared with those who own more mature businesses (50%).

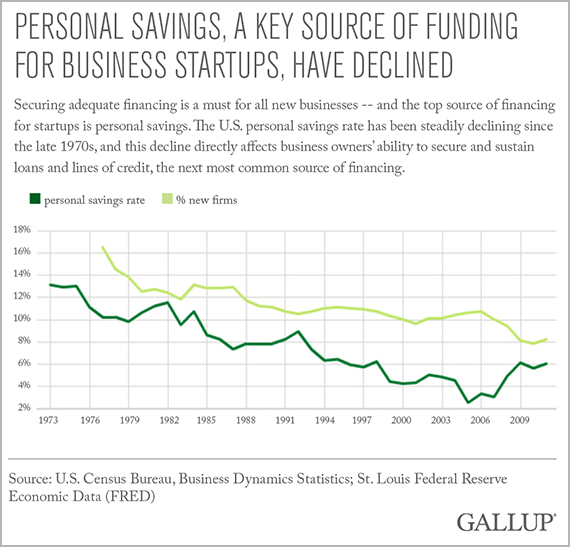

The U.S. personal savings rate -- personal savings as a percentage of disposable personal income or income after taxes that is not spent on personal consumption expenditures, interest payments, or transfer payments -- tracks the availability of the economic resources that prospective entrepreneurs depend on to finance new businesses.

The availability of personal savings also directly affects business owners' ability to secure and sustain loans and lines of credit, the next most common source of financing. Owners with little or no personal savings are less likely to convince banks that they can take on extra loan payments or provide collateral, such as a house or other high-value assets. And the U.S. personal savings rate, like the business startup rate, has been steadily declining since the late 1970s.

Personal savings rates, business startups decline

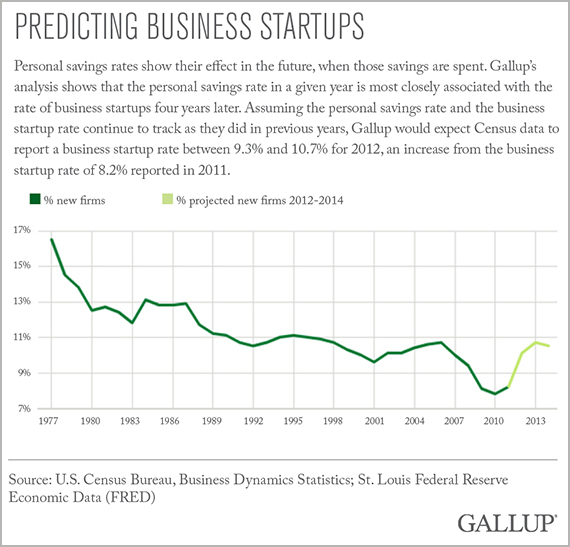

Money saved this year is, by definition, not spent this year. Personal savings rates for the current year, then, should show the greatest effect in a future year, when the accumulated savings are spent. Gallup's analysis shows that the personal savings rate in any given year is most closely associated with the rate of business startups four years later.

If the relationship observed between the personal savings rate and the business startup rate from 1977 to 2011 has continued in recent years, what can the available data tell us about the potential rate of business startups in current and future years? At this time, Census data on U.S. business startups is available through 2011 only. Assuming the personal savings rate and the business startup rate continue to track as they did from 1977 to 2011, Gallup would expect Census data to report a business startup rate between 9.3% and 10.7% for 2012, an increase from the business startup rate of 8.2% reported in 2011.

After a few years of stronger personal savings from 2009 to 2012, the personal savings rate fell in 2013 and 2014. This drop suggests that even if the personal savings rate and the rate of business startups pick up from 2013 to 2016, the U.S. may still see a decline in new business startups in the following years. The U.S. personal savings rate and the business startup rates remain well below the levels in the 1970s and earlier. Unless Americans start saving more -- and there is an uptick in the U.S. personal savings rate -- American entrepreneurship remains at risk.