Story Highlights

- Only 13% of U.S. adults have a digital wallet on their smartphone

- Competition is heating up between Apple, Google and PayPal

- Good news: The technology and the market are still developing

As U.S. consumers use more smartphones and mobile devices, it would seem natural for them to ditch their physical wallets and make digital payments whenever and wherever they could.

But not so fast. While digital wallets -- technology that allows users to store credit and debit cards, cash, and loyalty cards and coupons to make electronic purchases using a digital device, most often a smartphone -- were first introduced as far back as the 1990s, U.S. consumers have yet to readily accept them.

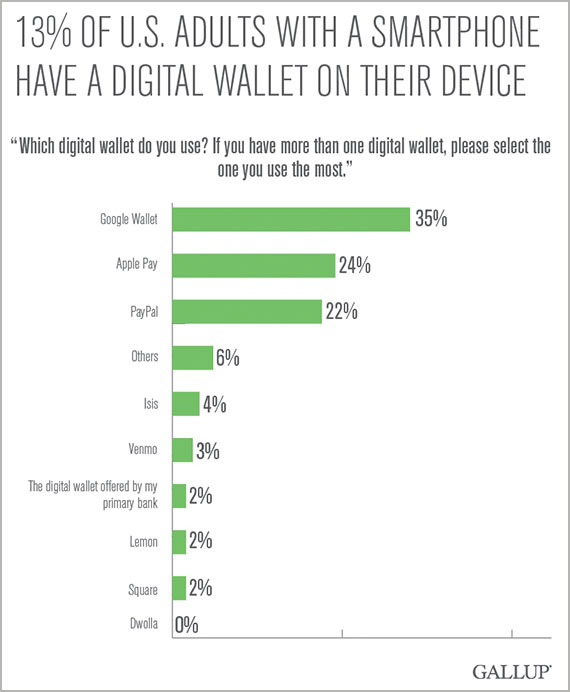

Though Apple is trying to change this trend with Apple Pay, Gallup analysis shows enthusiasm for digital wallets is still low. Only 13% of U.S. adults with a smartphone have a digital wallet on their device, and 76% of those who have a digital wallet have never used it or have almost never used it to make a purchase from a retailer in the past 30 days. Of the U.S. consumers using a digital wallet, men and millennials use it more than the rest of U.S. adults: 11% of men and 11% of millennials use it every time or almost every time if they can to make a purchase.

Among consumers who have digital wallets, 38% don't see any benefits of using the technology. What's more, nine out of 10 consumers who don't have a digital wallet say they are very unlikely or unlikely to start using one in the next 12 months (91%). This suggests that providers either lack a strong value proposition or aren't communicating it well to prospective customers. Unless this situation changes, it's hard to imagine many consumers moving beyond considering or experimenting with the technology to become loyal, long-term customers.

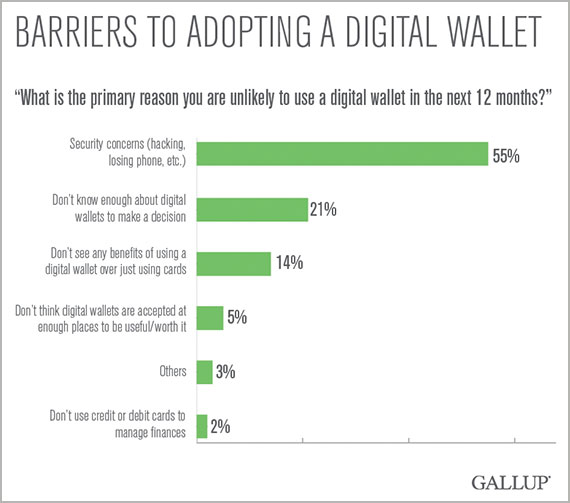

Consumers don't seem to be eager to start using digital wallets in the near future, with further analysis suggesting several reasons for their reluctance. More than half of nonusers cite security as a primary reason they're unlikely to use a digital wallet in the next 12 months (55%). Others don't know enough about the technology (21%) or see any benefits of using a digital wallet over just using credit cards (14%), while a few don't think they are accepted at enough places to make the technology useful or worth it (5%).

How Companies Can Gain the Greatest Number of Early Adopters

Though consumers' current enthusiasm for digital wallets is low, the competition in the market is becoming more intense. Apple has already shot to the No. 2 position in market share with the launch of Apple Pay, even though Google and PayPal have been in the digital wallet space longer.

Whether digital wallet companies are incumbents or startups -- and regardless of whether they're technology firms, retailers, banks or credit card companies -- every provider is looking for opportunities to win share from consumers and merchants. Amplified by the "network effect" -- which suggests that a good or service becomes more valuable as more people begin to use it -- the provider that gains the greatest number of early adopters could well dominate the marketplace. Here are some ways providers can create timely strategies to overcome barriers to adopting their digital wallets:

- Gain consumer trust on personal data security. Gallup's 2014 consumer trust study confirms that customers place some or a lot of trust in their banks to keep their personal data secure (91%), far more than they trust credit card companies (66%), cellphone platform providers (63%), cellphone carriers (59%), brick-and-mortar and online retailers (69% and 58%, respectively), and social networking services (23%). Though consumers' adoption of their bank's digital wallets is low, banks are well-positioned to overcome security concerns and increase use of their branded wallets. Given the complex network needed to make a digital wallet work, however, all companies involved -- including retailers, cellphone carriers, banks and credit card companies -- must strive to build trust among consumers and respond quickly to any security breaches. Consumers will remain reluctant to adopt this technology if they don't trust all parties involved to keep their personal data safe and secure.

- Educate consumers on what digital wallets are and how to use them. Following the launch of Apple Pay, many consumers have received emails and seen ads from companies and financial services firms encouraging them to adopt their company's product. Before more consumers become users, though, companies must help them understand what a digital wallet is and how to use it. Approaches include playing a video on how to use a digital wallet to customers waiting in line at a bank branch, or asking call center agents to close a call by asking customers if they are using a digital wallet, giving them the benefits of using one and answering any questions they might have about digital wallets. Retailers also could provide signage near checkouts explaining the benefits of a digital wallet and directing customers where to go for more information.

- Provide a clear value proposition. Almost all digital wallet providers claim they offer convenience, relieving customers of the need to carry multiple cards and remember separate passwords for each. However, 14% of nonusers are unconvinced by this claim. Companies must be innovative and provide different value propositions based on their unique competitive advantages to connect with consumers. For example, with knowledge about a customer's disposable income, credit card ownership, and purchasing preferences and frequencies, banks can offer more than a convenient method to make purchases. Banks can also serve as trusted financial advisers, helping customers understand how they are spending their money and how to make informed decisions about future purchases. Technology giants such as Google -- with its coming Android Pay platform -- and PayPal -- with its purchase of the Paydiant platform -- also want to maximize their strong technology and programming capabilities to provide customized digital wallets that developers can use to create their own apps. Customized apps would allow merchants to have their own uniquely branded digital wallets.

The lukewarm state of the digital wallet market is mainly driven by consumer reluctance to adopt this new technology, according to Gallup analysis. The good news for budding providers is that both the technology and the market are still developing, which offers every player a chance to win. Companies that can convince consumers to adopt their digital wallets -- by gaining their trust, educating them on how to use the technology and by providing a clear value proposition on how using it will benefit them -- will likely be the market leaders of the future.

Survey Methods

Results are based on a Gallup Panel Web study completed by 11,043 national adults, aged 18 and older, conducted Nov. 20-Dec.1, 2014, and a Gallup Panel Web study completed by 6,032 national adults, aged 18 and older, conducted Dec. 29, 2014-Jan. 16, 2015. The Gallup Panel is a probability-based longitudinal panel of U.S. adults whom Gallup selects using random-digit-dial phone interviews that cover landlines and cellphones. Gallup also uses address-based sampling methods to recruit Panel members. The Gallup Panel is not an opt-in panel and panel members do not receive incentives for participating. For results based on this sample, one can say that the margin of sampling error is ±1.3 percentage points, at the 95% confidence level. Margins of error are higher for subsamples. In addition to sampling error, question wording and practical difficulties in conducting surveys can introduce error or bias into the findings of public opinion polls.

Learn more about how the Gallup Panel works.