Story Highlights

- Community banks and credit unions have high customer engagement

- Yet their customers go to bigger banks for significant financial events

- "Good service" means having consultative conversations with customers

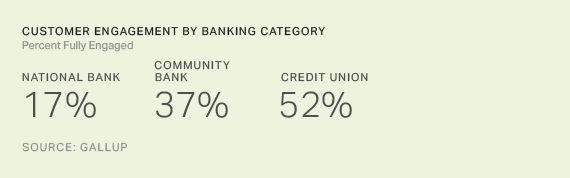

Community banks and credit unions have higher customer and member engagement than do national banks, according to Gallup data. Though 52% of credit union members and 37% of community bank customers are fully engaged, that figure drops to 17% for national banks.

The high level of customer or member engagement at community banks and credit unions doesn't spring from the nuts-and-bolts aspects of banking, such as rates, products, convenience or technology. Those basics are all necessary, but they don't provide a financial institution with sustainable advantages that differentiate it from its competitors. For community banks and credit unions, a real competitive advantage comes from customer engagement, which is a result not only of the products and services they provide but also of the way they make their customers feel.

Community banks and credit unions have a much larger "halo" of customer and member engagement around them than bigger banks, Gallup data show. This halo seems to come from the interpersonal bonds smaller banks build with their customers. These organizations have worked very hard -- and, as the data show, very successfully -- to help customers and members feel that they are valued and are getting personal attention. In turn, this helps them see the bank as part of the community and builds a sense of group identity and pride among customers and members.

Despite their positive experiences, customers of community banks and credit unions go to bigger banks to meet their most significant financial needs. That's a problem.

Community banks and credit unions have done the hard work of building engagement, but their current definition of "good service" doesn't meet their customers' and members' needs and goals. In failing to deepen their relationships with customers, these financial institutions are also failing to reap the benefits that come with engagement -- and they're failing their customers or members, too.

Going to Big-Money Banks for Big-Money Advice

In general, community banks and credit unions are right to believe that their efforts have paid off in engaged customers and members. But too often, those customers or members think of their banks or credit unions as merely hospitable places to store money. They don't consider them trusted financial advisers. They go to big-money banks for big-money advice, such as retirement, insurance and investment products.

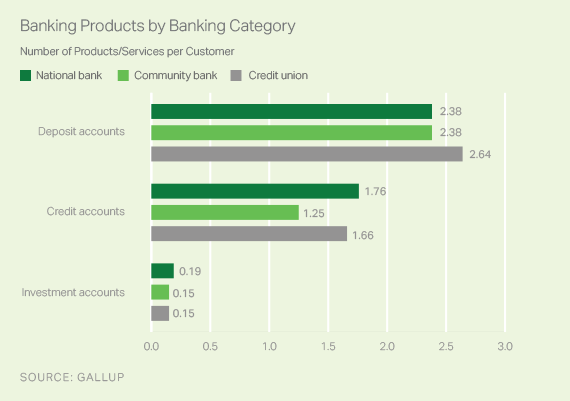

National banks may have a smaller percentage of engaged customers, on average, than community banks and credit unions do. But they do just as well as, if not better than, community banks and credit unions in several product/service categories, and they have a significant edge for credit products.

One reason national banks have an edge is that they are having more expansive conversations -- beyond deposit-related product discussions -- with their customers than community banks and credit unions are.

For example, though all banks have conversations with their customers about new accounts, at national banks, 2% of those conversations on average involve investment products, while only 1% did at community banks. And 8% of conversations with customers about new accounts at national banks involve credit products, compared with only 5% at community banks.

The quality of the conversation drives share of wallet -- and community banks and credit unions are having less-than-optimal numbers of conversations about key financial events and goals with their customers and members, in spite of their engagement advantage.

So these are the challenges for community banks and credit unions: How do they capitalize on their strong customer engagement to deepen relationships with their customers and members? How do they move beyond conversations about deposits to include high-value financial advice?

Customers and Members Want Meaningful Consultative Conversations

Gallup research suggests that for the most part, community banks and credit unions don't prompt consultative sales conversations with their customers and members. Failing to do so is a missed service opportunity for these institutions because they convert a significantly higher percentage of these conversations to more share of wallet than national banks do. When credit unions have a conversation with their members about an investment product, for example, their members are far more likely to buy than customers of national banks, given credit union members' engagement levels.

| National bank | Community bank | Credit union | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Had a sales conversation with a customer | 17% | 15% | 19% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Converted that conversation to a sale | 47% | 52% | 57% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Gallup | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Community banks and credit unions initiate conversations regarding new accounts or services about as often as bigger banks do, but they are more likely than the bigger banks to convert those conversations into a sale, Gallup data show. What's more, community bank customers and credit union members are more likely than national bank customers to bring these conversations to their bankers.

More than eight in 10 community bank customers (86%) and credit union members (88%) report they initiated an account discussion, compared with slightly more than six in 10 customers of national banks (61%). These findings suggest that customers and members are more than willing to have meaningful consultative conversations with their community bank or credit union about their financial needs and goals -- in fact, they actively seek them out.

More times than not, when customers and members of community banks and credit unions self-identify a need, they consider their community bank or credit union in meeting that need. But if a community bank or credit union doesn't fight to better serve its customers, those customers and members are willing to take that need to a bigger bank. To gain that business and win that share of wallet, community banks and credit unions need to be proactive in capitalizing on their higher engagement levels by prompting consultative conversations.

Community banks and credit unions have done the hard work of building trusting relationships with their members and customers. But to better serve them and expand their business with them, these institutions need to expand their definition of what constitutes good customer or member service. Providing good service goes far beyond making sales or meeting customers' and members' basic needs; it requires financial institutions to look out for their customers' and members' financial well-being, particularly in key financial decisions.

The irony is that customers may feel the folks at their community bank or credit union are better people -- but not better bankers -- than the folks at the national banks. By proactively helping customers and members better understand their financial needs and providing solutions aligned with those needs, community banks and credit unions can earn share of wallet by earning a reputation as trusted advisers. Under the new definition of "good service," failing to do so means failing the customer or member.

Survey Methods

Results are based on a Gallup Panel Web study completed by 19,354 national adults, aged 18 and older, conducted July 29-Aug. 18, 2015. The sample for this study was weighted to be demographically representative of the U.S. adult population using the most recent Current Population Survey figures. For results based on this sample, one can say that the maximum margin of sampling error is ±1 percentage point at the 95% confidence level. Margins of error are higher for subsamples. In addition to sampling error, question wording and practical difficulties in conducting surveys can introduce error or bias into the findings of public opinion polls.

Learn more about how the Gallup Panel works.