Story Highlights

- There's too much uncertainty, miscommunication and poor service

- Many customers do not get mortgages from their primary bank

- Engaging mortgage customers is a growth opportunity for banks

Getting a mortgage is often a stressful and unhappy experience for customers.

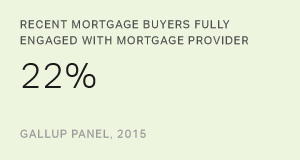

The process is so full of uncertainty, miscommunication and downright poor service that it's one of the least engaging of all the financial services that banks provide. Only about one in five recent mortgage buyers (22%) are fully engaged with their mortgage provider, Gallup finds, compared with 29% of customers who are fully engaged with their investment firm, 30% with their primary bank and 32% with their home, auto or life insurance provider.

Low engagement is bad news for mortgage providers, and it's likely hindering their growth. Fully engaged customers are essential for financial service institutions because they are emotionally and psychologically attached to the companies they do business with. They're the company's most loyal, vocal brand ambassadors, and they give the organization more of their time and new business.

How Customer Engagement Affects the Mortgage Business

When customers need a mortgage, they're more likely to turn to their main bank or credit union if they are fully engaged with the organization. Among customers with a mortgage, 39% of those who were fully engaged with their primary bank or credit union used that institution for their mortgage, compared with only 25% of actively disengaged customers, according to Gallup's 2014 Retail Banking Panel Study.

This means that many customers did not get their mortgage from their primary bank or credit union. Instead, many signed mortgages with banks with which they had no prior relationship. About a quarter of these customers subsequently began a retail relationship with the institution by opening a deposit account or credit card, and this decision appears to be largely influenced by engagement with the mortgage experience. Nearly half (46%) of fully engaged mortgage-only customers became retail customers of the bank holding their mortgage, compared with only 11% of actively disengaged mortgage-only customers.

Engaging mortgage customers also sets the stage for future growth. Fully engaged mortgage customers are more than twice as likely to return to the same bank or credit union for another mortgage when the need arises. Further, one in five customers report that they chose their mortgage provider based on a recommendation from a friend, family member or colleague -- but organizations must fully engage their customers if they want to earn these endorsements. When asked how likely they were to recommend their mortgage provider to a friend or family member, 93% of fully engaged customers say they were extremely likely, compared with only 3% of actively disengaged customers who say the same.

Low Engagement: A Missed Opportunity for Growth

Clearly, providing customers with an engaging mortgage experience is a key component of organic growth for financial institutions. Fewer than one in four customers are fully engaged with their mortgage provider. This is a big miss because when banks provide an engaging customer experience, they do more mortgage business among their retail customers and they increase retail business among mortgage customers. Some mortgage providers, such as mortgage-only banks, don't have to worry about retail cross-selling like commercial banks and credit unions do. But all mortgage providers should worry about attracting, engaging and retaining customers.

The mortgage process is a complex customer experience. Engagement or disengagement with a mortgage provider is determined by multiple factors, including service, a potentially complicated approval process and tactical elements related to closing on the loan.

Getting mortgage service right is not easy. It requires consistently executing a meticulously developed, complex customer strategy from start to finish to create more fully engaged customers. But the payoff -- such as more mortgage originations, cross-selling and repeat business -- makes it well worth the effort.

The next article will reveal how mortgage providers can increase their levels of fully engaged customers to win more business.

Survey Methods

Results are based on a Gallup Panel Web study completed by 1,627 national adults, aged 18 and older, conducted in July 2015. The Gallup Panel is a probability-based longitudinal panel of U.S. adults whom Gallup selects using random-digit-dial (RDD) phone interviews that cover landlines and cellphones. Gallup also uses address-based sampling methods to recruit panel members. The Gallup Panel is not an opt-in Panel, and Panel members do not receive incentives for participating. For results based on this sample, one can say that the maximum margin of sampling error is ±2.4 percentage points at the 95% confidence level. Margins of error are higher for subsamples. In addition to sampling error, question wording and practical difficulties in conducting surveys can introduce error or bias into the findings of public opinion polls.