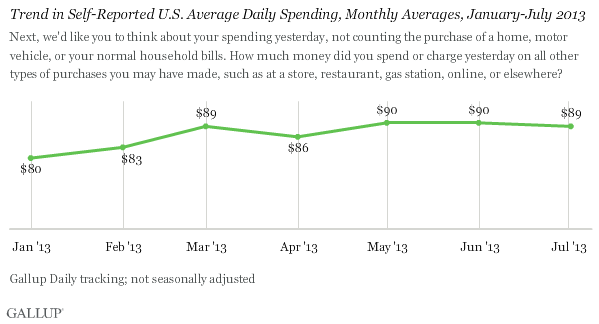

WASHINGTON, D.C. -- U.S. self-reported daily consumer spending was $89 in July, unchanged from the $90 of June and May. The relatively flat spending levels of the past five months are consistent with the weak GDP reports of the past three quarters and the lack of improvement Gallup finds in its Payroll to Population employment rate over the past couple of years.

These results are based on Gallup Daily tracking interviews, conducted by landline and cellphone, with more than 14,000 Americans from July 1-31. Gallup's consumer spending data are essentially a discretionary spending measure and are generally more closely related to chain-store sales and online sales than overall retail sales.

Spending began the year at $80 in January and $83 in February. Consumers opened their wallets some more in March, spending an average of $89, reflecting the normally expected seasonal spring increase in sales.

However, consumer spending has remained basically at that level since -- in the face of what are normally positive seasonal factors such as warmer weather, home improvement projects, and spring and summer travel. Longer-term, Americans' self-reported spending is much stronger than it was from late 2008 to late 2011, but continues to trail early 2008, before the recession gained momentum.

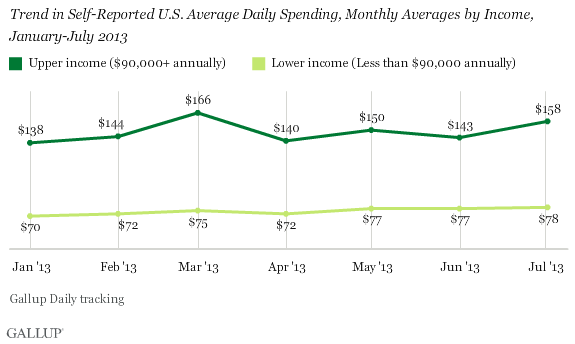

Spending Across Income Levels Also Relatively Flat

Upper-income spending inched up to $158 in July, from $143 in June and $150 in May. But the upper-income spending data tend to be more volatile due to the smaller sample sizes involved, and the overall trend seems to be essentially flat over the past five months -- with a peak of $166 in March and a low of $140 in April.

Lower- and middle-income spending averaged $78 per day in July, similar to the $77 per day in June and May, and the $75 in March. Spending by this group in 2013 has been in a relatively narrow range, from a high of $78 last month to a low of $70 in January.

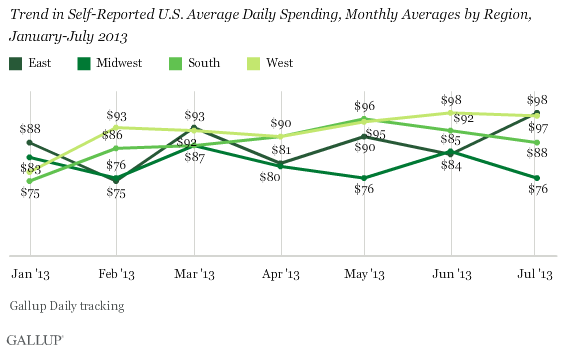

Spending Increase in the East Offset by Drop in the Midwest and South

Average daily consumer spending was highest in the East ($98) and West ($97) in July, while the South came in third at $88 and the Midwest last at $76. The West stayed in the lead by essentially matching its June spending level of $98, as it continues to enjoy an improving housing market in many cities.

Spending was up in the East in July, likely related to the Wall Street boom and improving conditions for financial institutions. Spending, however, declined in the South -- possibly related to some slowing in the energy industry in this part of the country during recent months. It dropped as well in the Midwest, which seems to be suffering from a continuing slowdown in manufacturing.

Implications

Even as Wall Street is reaching new record highs, questions remain about the strength of the Main Street economy. Gallup's self-reported spending results for July suggest the underlying economy remains fragile at best. This aligns with recent weak GDP reports, the lack of increase in full-time jobs with employers, the slight decline in economic confidence, and Friday's mixed, but also relatively weak, Bureau of Labor Statistics jobs report.

The reason spending hasn't in fact declined over the past several months may be that the Federal Reserve's efforts to flood the economy with money have not only been supportive of Wall Street, but also bolstered durable goods values in general, including housing and autos.

Still, at this point, Gallup's economic data do not support the idea of a significantly improving U.S. economy in the second half of the year. In turn, this suggests retailers may be disappointed with the Back-to-School spending season. The consumer spending outlook appears best in the East and the West, OK in the South, but not so good in the Midwest.

Gallup.com reports results from these indexes in daily, weekly, and monthly averages and in Gallup.com stories. Complete trend data are always available to view and export in the following charts:

Daily: Employment, Economic Confidence, Job Creation, Consumer Spending

Weekly: Employment, Economic Confidence, Job Creation, Consumer Spending

Read more about Gallup's economic measures.

View our economic release schedule.

Survey Methods

Results are based on telephone interviews conducted as part of the Gallup Daily tracking survey July 1-31, 2013, with a random sample of 14,717 adults, aged 18 and older, living in all 50 U.S. states and the District of Columbia, selected using random-digit-dial sampling.

For results based on the total sample of national adults, one can say with 95% confidence that the margin of sampling error is ±1 percentage point.

Interviews are conducted with respondents on landline telephones and cellular phones, with interviews conducted in Spanish for respondents who are primarily Spanish-speaking. Each sample of national adults includes a minimum quota of 50% cellphone respondents and 50% landline respondents, with additional minimum quotas by region. Landline and cell telephone numbers are selected using random-digit-dial methods. Landline respondents are chosen at random within each household on the basis of which member had the most recent birthday.

Samples are weighted to correct for unequal selection probability, nonresponse, and double coverage of landline and cell users in the two sampling frames. They are also weighted to match the national demographics of gender, age, race, Hispanic ethnicity, education, region, population density, and phone status (cellphone only/landline only/both, and cellphone mostly). Demographic weighting targets are based on the March 2012 Current Population Survey figures for the aged 18 and older U.S. population. Phone status targets are based on the July-December 2011 National Health Interview Survey. Population density targets are based on the 2010 census. All reported margins of sampling error include the computed design effects for weighting.

In addition to sampling error, question wording and practical difficulties in conducting surveys can introduce error or bias into the findings of public opinion polls.

For more details on Gallup's polling methodology, visit www.gallup.com.