Story Highlights

- Most U.S. investors have access to 401(k) plan and use it

- Yet 21% have recently taken a loan or early withdrawal

- Only 5% have lowered or stopped contributing to plan

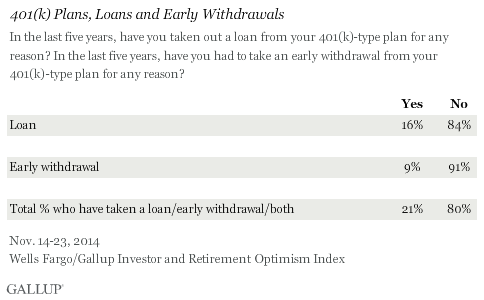

WASHINGTON, D.C. -- The majority of nonretired investors in the U.S. say their employer offers a 401(k) plan, and of these, 89% say they participate in it. Yet 21% of those who participate in such a plan say they have either taken out a 401(k) loan or even taken an early withdrawal from the plan in the last five years.

The latest findings from the Wells Fargo/Gallup Investment and Retirement Optimism Index show nonretired investors are generally enthusiastic about 401(k) plans, but there are some troubling signs and uncertainty regarding the investment vehicle. As long-term savings, 401(k) plans are not intended to be accounts from which contributors can make early withdrawals. However, not only have a fifth of investors tapped into 401(k) funds prematurely, but also barely more than half of those with a plan, 55%, say they understand the tax consequences of early 401(k) withdrawals "extremely well." Most of the rest, 40%, say they understand the consequences "somewhat well," and 5% say "not very well" or "not at all."

The fourth-quarter Wells Fargo/Gallup Investor and Retirement Optimism Index is based on a nationally representative telephone survey of 1,009 U.S. adults with $10,000 or more in investable assets, conducted Nov. 14-23, 2014. About two in five U.S. households have at least $10,000 in investments.

Most 401(k) Investors Actively Involved in Their Plan

With nearly 90% of nonretired investors saying they are participating in a 401(k) plan if their employer offers it, it is clear that 401(k) plans remain a popular investment option in American workplaces. Almost all investors with a plan (96%) say they are actively contributing to their plan, and 93% say they have reviewed their plan's performance in the last year. Another sign of the strength of the program is that, in a separate question, only 5% say they have lowered or stopped contributing to their 401(k) overall.

Bottom Line

Americans with $10,000 or more in investments are theoretically in a far better position than those with less or with nothing invested to get along without taking on debt. Yet 16% of this group reports having borrowed against their retirement plan in the past five years, and 9% have resorted to the more drastic option of making an early withdrawal. Five percent have done both.

Some of this may be attributable to Americans' putting less in liquid savings at a time of low interest rates, opting instead for maximizing what they can put in stock-based funds, such as those that make up the backbone of most 401(k) accounts. At a time when the U.S. savings rate is on the lower side of the historical range, investors with the capacity to save may need more guidance about how to save to avoid costly emergency measures, or having to take out loans or engage in early withdrawals.

Survey Methods

Results for the Wells Fargo/Gallup Investor and Retirement Optimism Index survey are based on questions asked Nov. 14-23, 2014, on the Gallup Daily tracking survey, of a random sample of 1,009 U.S. adults having investable assets of $10,000 or more.

For results based on the entire sample of investors, the margin of sampling error is ±3 percentage points at the 95% confidence level. All reported margins of sampling error include computed design effects for weighting.

In addition to sampling error, question wording and practical difficulties in conducting surveys can introduce error or bias into the findings of public opinion polls.

Learn more about how the Wells Fargo/Gallup Investor and Retirement Optimism Index works.