Story Highlights

- In U.S., 26% began saving for retirement before age 25

- Average age investors started saving is 29

- Seven in 10 investors think they could save more if they tried

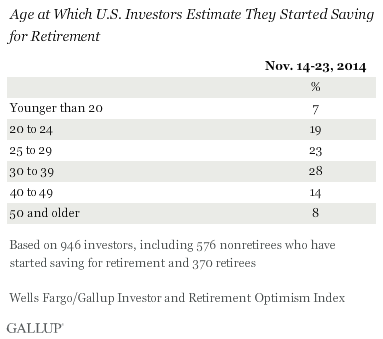

PRINCETON, N.J. -- Twenty-six percent of investors in the U.S. report that they started saving for their retirement before they turned 25, including 7% who had the foresight -- or, more likely, the adult guidance -- to start before they turned 20.

Another 23% began between the ages of 25 and 29, meaning about half of today's investors started the process of saving for retirement before turning 30. Investors who start saving for retirement by their 20s are positioned to enjoy tremendous gains because of the effect of compound interest in long-term investing, often termed "snowball savings."

While the remainder of investors might have missed these prime years for maximizing the snowball effect, a large segment -- 28% of all investors -- say they first started saving at some point in their 30s. Relatively few, 14%, waited until their 40s or until they were 50 or older (8%).

This question was asked of all retired investors and the 91% of nonretired investors who say they are saving for their retirement. The average age at which all of these investors started saving is 30, while it is slightly higher among retirees (age 35) than nonretirees (age 29).

The findings are from the latest Wells Fargo/Gallup Investor and Retirement Optimism Index survey of U.S. adults who have at least $10,000 invested in stocks, bonds or mutual funds. The survey was conducted Nov. 14-23.

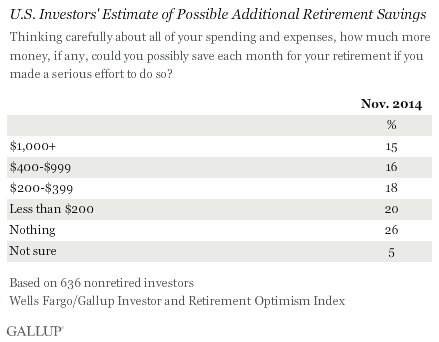

Most Investors Could Save More

About a quarter of nonretired investors who are currently saving for their retirement say they could not possibly save any more each month than they already do. Most of the rest (69%), however, believe they could -- with the median additional estimated savings among this group being $250 more each month.

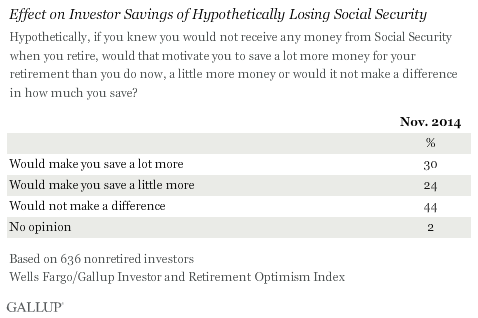

Another indication that investors could devote more resources to their retirement if they had to comes from a question asking, hypothetically, how knowing that they would not receive any money from Social Security in retirement might influence their savings behavior. Three in 10 say this scenario would motivate them to save a lot more money for their retirement, and another 24% say it would motivate them to save a little more. Less than half, 44%, say it would not make a difference.

Investors' responses to this question indicate that many are counting on Social Security as a safety net for at least some of their retirement security. More importantly, their answers reveal that despite past Wells Fargo/Gallup research showing that 38% of nonretired investors fear they are not saving enough for retirement, the truth is many probably could be saving more with careful budgeting. While there is little risk that the government will deny any of today's investors all of their Social Security benefits, additional savings is probably warranted for many, as the agency itself projects it will only be able to pay 76% of benefits come 2037 without additional revenue.

Bottom Line

In an ideal world, every employed American could start saving for retirement in his or her early 20s, using tax-advantaged accounts to shelter at least 10% of his or her income and earning interest that well outpaces inflation. Unfortunately, the reality usually falls short of these goals, and as a result, just two in five adult Americans even have the $10,000 in investments needed for inclusion in the Wells Fargo/Gallup Investor and Retirement Optimism Index. Of these investors, half tell Gallup they started saving for their retirement in their 20s.

By this point in the holiday season, spare cash can be hard to come by, but for those who have a little extra and do not yet have a retirement account, learning about compound interest could provide them the motivation to start saving. And for those investors who believe they can squeeze out more savings each month, now is the time to increase their 401(k) contributions for next year or make a catch-up contribution for 2014 if eligible.

Survey Methods

Results for the Wells Fargo/Gallup Investor and Retirement Optimism Index survey are based on questions asked Nov. 14-23, 2014, on the Gallup Daily tracking survey, of a random sample of 1,009 U.S. adults having investable assets of $10,000 or more.

For results based on the entire sample of investors, the margin of sampling error is ±3 percentage points at the 95% confidence level.

In addition to sampling error, question wording and practical difficulties in conducting surveys can introduce error or bias into the findings of public opinion polls.

Learn more about how the Wells Fargo/Gallup Investor and Retirement Optimism Index works.