Story Highlights

- A third of working investors with a 401(k) say they need advice

- One-on-one with financial professional rated most effective

- One-quarter rate employer subpar for guiding workers on 401(k)s

PRINCETON, N.J. -- U.S. investors who have access to a 401(k)-type plan at work consider live meetings with human advisers -- particularly one-on-one meetings with a financial professional -- to be the best way to get information about how to manage their retirement plans. Far fewer say sending information through mobile messaging or posting on social media is "highly effective." Various forms of written communication fall in between.

These findings are from the Wells Fargo/Gallup Investor and Retirement Optimism Index 2015-first quarter survey, conducted Jan. 30-Feb. 9. For this survey, investors are defined as U.S. adults who have at least $10,000 invested in stocks, bonds or mutual funds. About three in four employed investors report they have access to a 401(k)-type retirement savings plan at work. Beyond standard 401(k) plans, that could also mean 403(b) plans commonly used by teachers and other public employees.

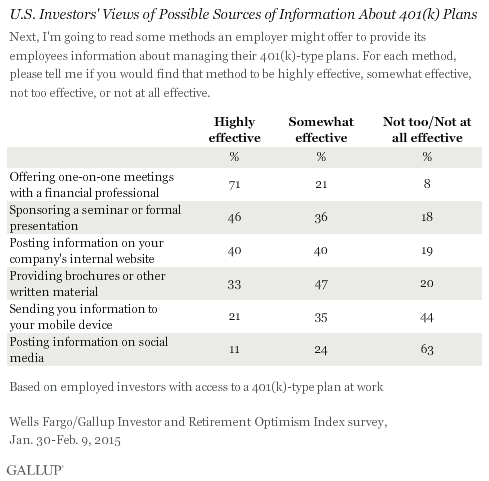

According to these investors, one-on-one meetings with a financial professional are the best way employers can provide employees information about managing their 401(k)-type plans, with 71% calling these highly effective. Employer-sponsored seminars or formal presentations rank second, at 46%, followed by information posted on a company website, at 40%. Confidence drops to 33% for written material such as brochures, 21% for information sent to employees' mobile devices and 11% for information posted on social media.

In terms of the total percentage rating each approach at least somewhat effective, all but social media (at 35%) receive majority confidence, ranging from 92% for one-on-one meetings to 56% for information pushed to mobile devices.

Employed 401(k) investors give their employer generally positive reviews of the job it does in providing employees with information about managing their plan, with about three in four rating it excellent (31%) or good (43%). However, one in four indicate their employer could be doing much better, rating its performance only fair (19%) or poor (6%).

401(k) Investors Need More Help in Picking, Changing Investments

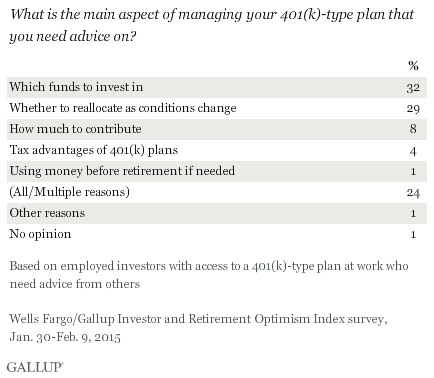

Close to two-thirds of employed investors who currently have a 401(k)-type plan say they can manage their plan by themselves, but 35% say they need advice. Given five areas of investing to choose from, most in the latter group identify knowing which funds to invest in (32%) or knowing when to reallocate funds (29%) as the area they most need help with. While relatively few choose knowing how much to contribute, understanding the tax advantages or tapping retirement money early, 24% say they need help on all or multiple issues.

Bottom Line

Although sponsored by employers, 401(k)-type plans put the onus on workers to save and invest for their retirement using these tax-advantaged accounts. Most investors indicate they are pretty comfortable managing their plan on their own, but a full third say they need advice. A natural place to get that advice is in the workplace, where the employer serves as the intermediary between the investor and the company managing the funds. Most investors are complimentary of the job their employer does of helping workers with the important task of managing their 401(k). But one in four think their employer is not doing a very good job, representing an important information gap that warrants attention.

In December, the Wells Fargo/Gallup Investor and Retirement Optimism Index survey found just 18% of U.S. investors saying they want more financial advice from their employer, per se. Likewise, most employers probably do not want to take responsibility for advising employees about critical financial decisions such as what to invest in and when to reallocate investments in response to market conditions. But given investors' reported needs and views about various sources of information, employers could do more to connect workers who are seeking advice with financial professionals who can personally guide them.

Survey Methods

Results for the Wells Fargo/Gallup Investor and Retirement Optimism Index survey are based on questions asked Jan. 30-Feb. 9, 2015, on the Gallup Daily tracking survey, of a random sample of 1,011 U.S. adults having investable assets of $10,000 or more.

For results based on the entire sample of investors, the margin of sampling error is ±3 percentage points at the 95% confidence level.

For results based on the 416 nonretired investors who have access to a 401(k) plan at work, the margin of sampling error is ±6 percentage points at the 95% confidence level. For results based on the 370 investors who participate in their employer's 401(k) plan the margin of sampling error is ±6 percentage points at the 95% confidence level. For results based on the 182 investors who say they need help in managing their 401(k) plan, the margin of sampling error is ±9 percentage points at the 95% confidence level.

In addition to sampling error, question wording and practical difficulties in conducting surveys can introduce error or bias into the findings of public opinion polls.

Learn more about how the Wells Fargo/Gallup Investor and Retirement Optimism Index works.