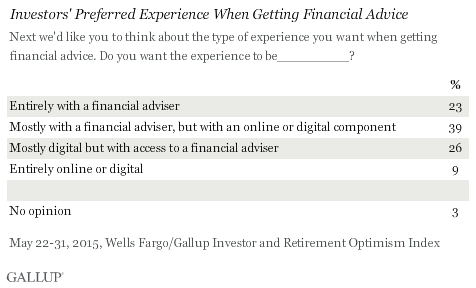

PRINCETON, N.J. -- U.S. investors see online and digital investment tools as complements to the advice they get from a personal financial adviser. Nearly two in three investors say they prefer to get financial advice from both sources, including 39% who want advice to come mostly from advisers and 26% who want it to come mostly from digital tools.

While fewer investors want to stick to a single source of financial advice, many more favor using just an adviser (23%) than favor relying solely on digital tools (9%).

The results are based on the May 22-31 Wells Fargo/Gallup Investor and Retirement Optimism Index survey. For this survey, investors are defined as U.S. adults who have at least $10,000 invested in stocks, bonds or mutual funds, or in a self-directed IRA or 401(k).

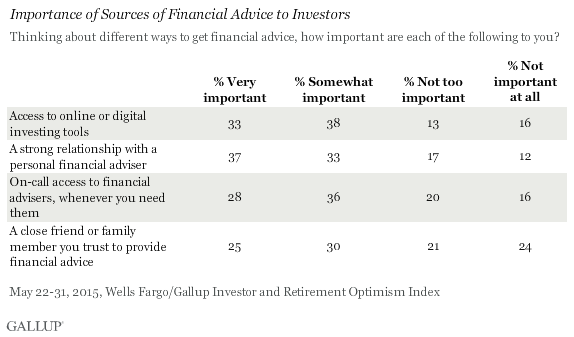

Although most investors like using both advisers and digital tools, they clearly tilt in favor of human advice. A combined 62% prefer getting financial advice exclusively (23%) or mostly (39%) from a personal financial adviser, whereas a combined 35% prefer mostly (26%) or exclusively (9%) digital advice. Also, when asked to choose between three sources of advice, 50% opt for a strong relationship with a financial adviser, 24% for access to state-of-the-art online or digital investing tools, and 19% for access to on-call financial advisers.

Despite these preferences, investors widely use digital investment sources, with three-quarters saying they use digital tools a lot (19%) or a little (57%). Eighty-five percent of investors report that their primary financial institution offers a variety of online investing tools and services.

Also, investors are just as likely to say digital sources are important as they are to say this about a personal financial adviser when asked to rate each item separately. Specifically, 71% say access to online or digital investing tools is very or somewhat important to them, while 70% say the same about having a strong relationship with a personal financial adviser. Having on-call access to financial advisers or having a trusted friend or family member as an adviser is less important to investors.

Digital Advice Has Greater Reach Among Younger Investors

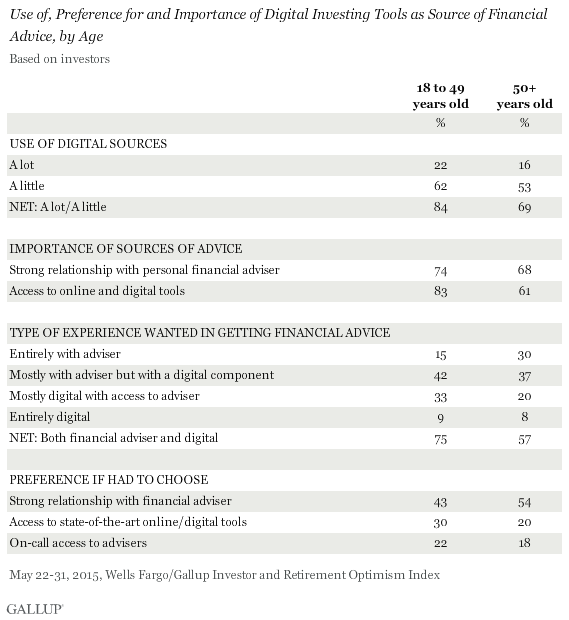

Investors as a whole tend to skew older, but within the investor group, younger investors are more likely than older investors to use digital sources of investment advice, to rate them as important, to say they prefer to use them over other potential sources and to prefer a mixture of digital and human sources of advice.

- Eighty-four percent of investors younger than 50 use digital sources of investment advice a lot or a little, compared with 69% of those aged 50 and older.

- Whereas 61% of older investors say access to digital sources of advice is important to them, a much higher 83% of younger investors rate such access as important.

- Seventy-five percent of younger investors prefer a mix of digital and human sources of investment advice, compared with 57% of older investors. Older investors (30%) are twice as likely as younger investors (15%) to want financial advice entirely from a financial adviser.

Even though younger investors are more positively disposed toward digital investing tools than older investors are, younger investors are not necessarily ready to abandon financial advisers. The majority of younger investors still prefer an experience that relies mostly (42%) or exclusively (15%) on financial advisers. And if forced to choose, more younger investors, 43%, opt for a strong relationship with a financial adviser than opt for access to state-of-the-art electronic investing tools (30%). Also, nearly three in four younger investors say a strong relationship with a financial adviser is important to them, though that is less than the 83% who say access to digital investing tools is important.

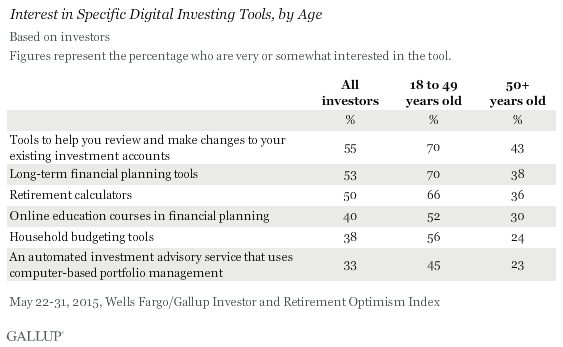

The survey also finds large and consistent differences by age when investors are asked about interest in a variety of specific digital investing tools. These are apparent in tools that help with long-range matters -- which may be of less relevance to older investors -- including retirement calculators and long-term financial planning tools, but also in tools that address current financial matters like household budgeting and online access to investment accounts.

Implications

Technology has improved Americans' lives in many ways, and that includes getting access to financial advice. Internet websites and smartphone apps now put a wide-ranging set of investment tools at investors' fingertips. Most U.S. investors report that they use these digital tools, and they generally regard them as an important source of financial advice.

But investors still value the advice they get from personal financial advisers, with most preferring a mix of financial advice from a dedicated adviser along with access to digital investing tools. Thus investors tend to see financial advisers and digital investment tools as complementary.

Younger investors' greater likelihood to use digital investing tools and to see them as important suggest reliance on digital tools will only increase in the future. However, because younger investors still very much favor a role for financial advisers, professional advisers will likely continue to play a prominent role in helping Americans make their investing decisions for the foreseeable future.

Survey Methods

Results for the Wells Fargo/Gallup Investor and Retirement Optimism survey are based on questions asked May 22-31, 2015, on the Gallup U.S. Daily survey, of a random sample of 1,009 U.S. adults having investable assets of $10,000 or more. For results based on the total sample of investors, the margin of sampling error is ±4 percentage points at the 95% confidence level. All reported margins of sampling error include computed design effects for weighting.

Each sample of national adults includes a minimum quota of 50% cellphone respondents and 50% landline respondents, with additional minimum quotas by time zone within region. Landline and cellular telephone numbers are selected using random-digit-dial methods.

Learn more about how the Wells Fargo/Gallup Investor and Retirement Optimism Index works.