Story Highlights

- Thirty-eight percent of investors have written financial plan

- Many more nonretired investors have plan now than in 2011

- About half of investors are following their plans very closely

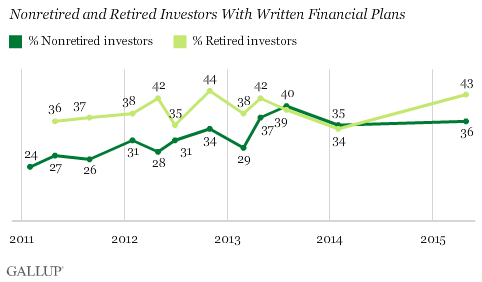

PRINCETON, N.J. -- Thirty-eight percent of U.S. investors have a written financial plan to help them achieve their investment and retirement goals. Retired investors (43%) are more likely than nonretired investors (36%) to have a written financial plan, as is typically the case. However, the percentage of nonretired investors with a written plan is up significantly since early in 2011 (24%).

A financial plan typically consists of investors' goals -- commonly for retirement savings, but also for college savings, insurance needs, taxes and major purchases. Having a written plan with specific goals and formal steps to take should increase the likelihood that people will achieve those goals. Those without a formal written plan may instead have vague notions as to what their financial aims are and how to attain them. Still others may not have even thought about long-range financial matters.

In three separate surveys conducted in 2011, an average 26% of nonretired investors said they had a written financial plan. That increased to an average 31% in 2012 and 35% in 2013 and has been at about that level since.

There has been a very slight increase among retired investors since 2011, from an average 37% in 2011 to an average 39% since then.

The rise in the percentage of both nonretired and retired investors with written financial plans coincides with the long-running U.S. stock bull market, the drop in the U.S. unemployment rate, as well as generally improving confidence in the U.S. economy.

The results are based on the Wells Fargo/Gallup Investor and Retirement Optimism Index survey, conducted May 22-31. The survey defines investors as those with $10,000 or more in investable assets.

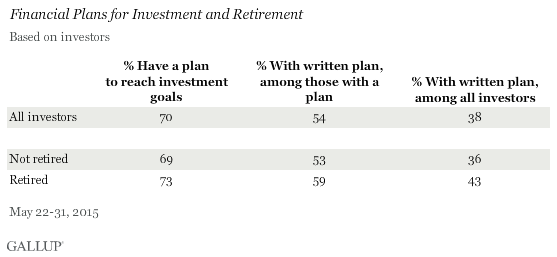

Overall, 70% of investors say they have a financial plan, but barely more than half of those with a plan, 54%, say it is a written plan. Those figures translate to 38% of all U.S. investors having a written plan. Retired investors are a bit more likely than nonretired investors to say they have a plan and to say it is a written plan.

Investors who do not have a written plan are most likely to cite a lack of time (29%) or not having thought about it (27%) as a reason they do not have a written plan. Another 18% say they do not find written financial plans to be useful.

Most Investors With Plan Follow It Closely, Are Confident in It

Having a financial plan is a key first step in reaching one's investment goals, but those goals will likely be harder to achieve if investors do not follow the plan. The majority of investors with a written financial plan, 53%, say they follow that plan "very closely." Another 39% say they follow it "somewhat closely."

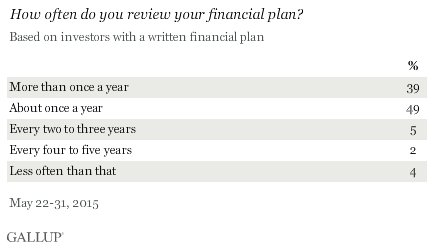

One way investors can keep on track with their financial plan is to review it on a regular basis. The vast majority of investors with a written financial plan, 88%, say they review it at least annually, including 39% who do so more than once a year.

Another way for investors to stay on track with their plan is to enlist the help of a professional adviser. The vast majority of investors with a written plan, 74%, say they developed the plan with the help of an investment adviser, including 80% of substantial investors and 61% of less substantial investors. Substantial investors are those with $100,000 or more of investable assets.

Investors with a written plan tend to be confident that it is adequately designed to help them reach their goals. Four in 10, 42%, are highly confident of this, with another 48% somewhat confident.

Retirement Is Common Focus of Financial Plans

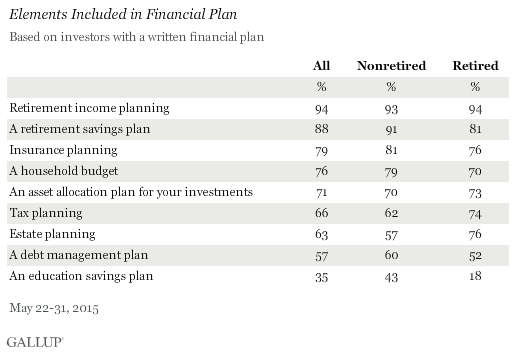

Nearly all investors with a written plan include retirement as a key component of their saving and investing plan. Ninety-four percent say their financial plan includes retirement income planning, and 88% say it includes a retirement savings plan.

After retirement, other key focus areas are insurance planning, a household budget and an asset allocation plan for investments. Reflecting the generally older age of investors, just 35% say their financial plan includes an education savings plan. Forty-three percent of nonretired investors have education savings as a component of their financial plan, compared with 18% of retired investors.

Retired (76%) and nonretired (57%) investors also differ in the extent to which their financial plan includes estate planning.

Implications

Although most U.S. investors say they have a financial plan, fewer than four in 10 have gone the extra step to develop a written financial plan. However, that percentage has been growing in recent years. A written plan is a key tool to help investors define their goals and spell out specific steps needed to achieve those goals. The act of developing a clearly defined written plan likely keeps investors more on track for their goals than if they did not have such a plan. Those who do have a written plan appear to be more committed to achieving their goals than those who do not have such a plan -- most with a written plan have employed a financial adviser to help develop it, say they follow it at least somewhat closely and say they review it at least annually.

Survey Methods

Results for the Wells Fargo/Gallup Investor and Retirement Optimism Index survey are based on questions asked May 22-31, 2015, on the Gallup Daily tracking survey, of a random sample of 1,005 U.S. adults having investable assets of $10,000 or more.

For results based on the entire sample of investors, the margin of sampling error is ±4 percentage points at the 95% confidence level.

In addition to sampling error, question wording and practical difficulties in conducting surveys can introduce error or bias into the findings of public opinion polls.

Learn more about how the Wells Fargo/Gallup Investor Optimism and Retirement Index works.