Story Highlights

- In-branch ATMs can help bridge the migration to digital channels

- Banks should make mobile banking more akin to online banking

- Online account openings should include a personal component

This is the second article in a two-part series.

More than ever before, banking customers want to use digital channels.

In fact, nearly six in 10 banking customers (56%) prefer more of a digital than a personal relationship with their bank, according to a Gallup study.

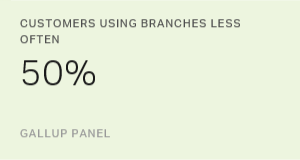

To meet customers' digital wants and needs -- and to save money -- many banks are aggressively expanding digital channels. But so far, this is not going smoothly; customers are not abandoning physical channels. Although banks are offering more channels, they are not realizing desired outcomes such as reduced costs and higher customer engagement.

In part, this reflects customers' preferences. Even among customers who prefer digital to personal banking, 38% would only consider using a bank that offers physical branches. As banks promote digital channels, they cannot simply abandon branches.

But banks are also partially at fault. When banks are hesitant to fully embrace their digital evolution, they are left with a burdensome and costly channel infrastructure while maintaining expensive branches.

In addition, many banks are biting off more than they can chew -- building a vast omnichannel network aimed at allowing customers to do everything they want in every single channel. The problem is, providing mediocre customer experiences across a variety of channels only hurts banks because channel satisfaction drives customer outcomes more than access to multiple channels does.

So, how can banks migrate customers to digital channels in an engaging, lucrative way?

Find Digital-Ready Customers

First and foremost, banks need to make channel satisfaction a higher priority than offering a plethora of channels. Banks should focus on providing perfect service in each channel interaction.

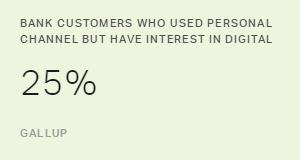

Banks also need to know which customers are ready to move to digital channels. Among customers who satisfied a need via a personal channel in the past three months, 25% said they were interested in accomplishing the same task digitally. This presents a win-win opportunity: By proactively finding digital-ready customers and encouraging them to explore online and mobile options, banks give customers the benefits they seek while reducing service costs.

Gallup finds that customers who prefer a more digital relationship than they currently have tend to be men, millennials and Gen Xers, students, and full-time employees with higher annual household incomes. In addition, highly educated customers are more likely to prefer digital over personal banking.

On the other hand, customers who prefer personal to digital banking tend to be women, baby boomers and traditionalists, part-time and retired workers, residents in the Northeast and Midwest, and those with a high school education or less. Customers who prefer a more personal relationship than they currently have are the most challenging customers to migrate to digital channels; these customers tend to be women with a high school education or less.

Ease the Transition to Digital

Here are strategies that banks can use with digital-ready candidates to encourage and ease the transition.

Walk customers across the ATM bridge. Think of ATMs and in-branch kiosks as a "bridge" to other digital channels -- especially for customers who are primarily branch users. To point customers to ATMs, kiosks and other digital resources, banks should provide targeted awareness-building activities and education, including walking customers through the process when necessary. This tactic not only reduces the need for future human interaction but also helps customers feel more comfortable with online and mobile banking.

Keep enhancing mobile banking. Smartphones have become the hub of daily communication. But banks don't always take advantage of this resource -- especially when it comes to targeting customers who are not tech-savvy and providing mobile options beyond basic banking. Banks should improve usability and functionality by:

- creating a mobile user experience more similar to online banking

- leveraging advanced biometric security systems to increase customers' comfort with activities such as paying bills and making mobile deposits

- allowing greater flexibility in policies, such as higher limits on check deposits or currency conversions

- creating a superior omnichannel experience by integrating click-to-call, click-to-chat and video banking options

Offer personal interactions during digital account openings. To some banks, digital account openings are considered the "final frontier" of the migration to digital banking, given their inherent complexities. Instead, banks should view digital account openings as an opportunity to complement digital banking with personal interaction by providing options for personal service via chat, video or phone. Even tech-savvy customers may want the opportunity to interact with associates during the setup process to ask questions, discuss options and address concerns. Without a human touch, banks risk losing the immediate sale as well as opportunities for cross-selling and upselling.

Bailey Nelson contributed to this article.

Survey Methods

Results are based on a Gallup Panel web study completed by 6,032 national adults, aged 18 and older, conducted Dec. 29, 2014, to Jan. 16, 2015. The sample for this study was weighted to be demographically representative of the U.S. adult population, using the latest Population Survey figures. The Gallup Panel is a probability-based longitudinal panel of U.S. adults whom Gallup selects using random-digit-dial phone interviews that cover landlines and cellphones. Gallup also uses address-based sampling methods to recruit Panel members. The Gallup Panel is not an opt-in panel, and Gallup Panel members do not receive incentives for participating. For results based on this sample, the margin of sampling error is ±1.3 percentage points at the 95% confidence level. Margins of error are higher for subsamples. In addition to sampling error, question wording and practical difficulties in conducting surveys can introduce error or bias into the findings of public opinion polls.