Story Highlights

- Half of investors rely on financial firms' websites or mobile apps

- Majorities check their statements online

- Most investors aged 50+ still rely mainly on phone and branch office

PRINCETON, N.J. -- U.S. investors split into two camps when it comes to the method they prefer for interacting with the financial services firm that handles their investments. Fifty percent of investors say they rely mainly on the firm's website (40%) or mobile app (10%), while a combined 47% still turn to traditional methods including the branch office (25%) or telephone (22%).

| U.S. investors | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Website | 40 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Branch office | 25 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Telephone | 22 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Mobile app | 10 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| (All equally) | 1 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| No opinion | 2 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Wells Fargo/Gallup Investor and Retirement Optimism Index, May 13-22, 2016 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

More broadly, investors divide roughly into thirds when it comes to reliance on mobile apps and other online tools and services. About a third (31%) say they do everything they possibly can online, while 38% say they only do some things online and 31% do very little.

Naturally, there is a strong generational aspect to these preferences. Most strikingly, a combined 69% of investors aged 18 to 49 say that a website or mobile app is the most important means for them to interact with their primary financial firm, whereas 59% of older investors cite the telephone or branch office. Similarly, while 43% of younger investors say they do everything they possibly can online, an equal proportion of older investors, 45%, say they do very little online.

| 18 to 49 | 50+ | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| % | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Most important channel for interacting with financial firm | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Website | 53 | 31 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Branch office | 18 | 29 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Telephone | 12 | 30 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Mobile app | 16 | 6 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| TOTAL WEBSITE/MOBILE APP | 69 | 37 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| TOTAL TELEPHONE/BRANCH OFFICE | 30 | 59 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Orientation to online tools and mobile apps | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Do everything you possibly can online | 43 | 20 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Do only some things online | 41 | 35 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Do very little online | 16 | 45 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Wells Fargo/Gallup Investor and Retirement Optimism Index, May 13-22, 2016 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

These findings are from the second quarter Wells Fargo/Gallup Investor and Retirement Optimism Index survey, conducted in May. The survey reflects the views of U.S. investors with $10,000 or more invested in stocks, bonds or mutual funds.

Investors Use Web for Routine Financial Tasks, but Not Advice

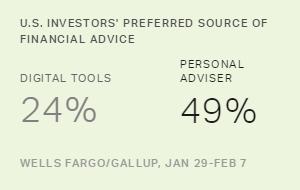

Despite these general orientations toward technology, about six in 10 investors indicate they do a variety of routine financial tasks online. This includes reviewing their investment statements, reviewing account fees and transferring money between funds. Fewer than half, however, say they use an online method to rebalance (45%) or make changes to their investments (46%) or to calculate their retirement needs (46%). And fewer still, just 24%, say they go online for investment advice.

| Online method | Some other method | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| % | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Reviewing account fees | 62 | 35 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Transferring money between funds | 61 | 33 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Reviewing your investment statements | 60 | 37 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Making changes to your investments | 46 | 49 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Calculating your retirement needs | 46 | 48 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Rebalancing your investments | 45 | 49 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Getting investment advice | 24 | 70 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Note: "Never do task" responses not included | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Wells Fargo/Gallup Investor and Retirement Optimism Index, May 13-22, 2016 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

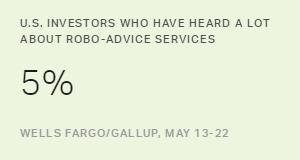

In line with the low percentage of investors who seek investment advice online, the survey found that just 5% of investors are highly familiar with or have already used robo-advice -- that is, online advisory services that rely on computer algorithms to select and manage customers' investments.

Some of the variation in the percentage of investors using an online vs. "some other" method to do things like rebalance or calculate their retirement needs could reflect lower proportions of investors engaging in these activities at all; however, no more than 5% volunteered in the survey that they never engage in these tasks.

In line with their general preferences for interacting with their primary investing firm, majorities of investors younger than 50 say they use the web for almost all of the investing activities tested, whereas less than half of those 50 and older do so.

| 18 to 49 | 50+ | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| % | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Reviewing account fees | 79 | 49 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Transferring money between funds | 80 | 47 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Reviewing your investment statements | 80 | 47 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Making changes to your investments | 64 | 34 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Calculating your retirement needs | 63 | 34 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Rebalancing your investments | 60 | 33 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Getting investment advice | 30 | 20 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Wells Fargo/Gallup Investor and Retirement Optimism Index, May 13-22, 2016 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Investors who have a dedicated financial adviser tend to be less likely to handle various investing tasks for themselves online, but this does not explain the large age differences described above. First, younger investors are only slightly less likely than those 50 and older to have such an adviser. Moreover, the age gaps persist among investors who have and who do not have their own adviser.

Bottom Line

While the internet is ubiquitous in people's lives and offers numerous ways for investors to stay on top of their investments, nearly half of investors still rely mainly on in-person interactions, or at least the familiarity of the telephone, to conduct their investment transactions. However, a sea change is on the horizon, because investors younger than 50 show tremendous willingness not only to monitor their investments online but also to use digital tools to move money around and calculate their retirement needs.

Close to half of younger investors describe themselves as the kind of people who do everything they can online. The one digital offering they still resist is getting their investment advice through a computer or mobile app, meaning human advisers -- whether working as personal financial advisers or in call centers -- will continue to play an important role in investors' lives.

Survey Methods

Results for the Wells Fargo/Gallup Investor and Retirement Optimism Index survey are based on questions asked May 13-22, 2016, on the Gallup Daily tracking survey, of a random sample of 1,019 U.S. adults having investable assets of $10,000 or more.

For results based on the total sample of investors, the margin of sampling error is ±4 percentage points at the 95% confidence level. All reported margins of sampling error include computed design effects for weighting.

Each sample of national adults includes a minimum quota of 60% cellphone respondents and 40% landline respondents, with additional minimum quotas by time zone within region. Landline and cellular telephone numbers are selected using random-digit-dial methods.

Learn more about how the Wells Fargo/Gallup Investor and Retirement Optimism Index works.