Story Highlights

- Nine in 10 employed investors view their 401(k) plan positively

- Majority seek allocation advice from personal financial adviser

- Younger plan holders also rely on Internet, family advice

PRINCETON, N.J. -- The vast majority of employed U.S. investors who participate in a 401(k) savings plan, the primary means of retirement savings for many working Americans, view it positively. Nine in 10 investors say they are satisfied with their own 401(k) plan as a tool for saving for their retirement, including 44% who are "very" satisfied and 47% who are "somewhat" satisfied. Just 9% are somewhat or very dissatisfied.

| Total participants% | Investments of $100,000+% | Investments of less than $100,000% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Very satisfied | 44 | 46 | 43 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Somewhat satisfied | 47 | 47 | 47 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Somewhat dissatisfied | 7 | 6 | 7 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Very dissatisfied | 2 | 1 | 3 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Jan. 29-Feb. 7, 2016 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Wells Fargo/Gallup Investor and Retirement Optimism Index | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Satisfaction is just as high among those with less than $100,000 invested (90%) as it is among higher-asset investors (93%), indicating the 401(k)'s egalitarian appeal.

These findings are from the latest Wells Fargo/Gallup Investor and Retirement Optimism Index survey, conducted Jan. 29-Feb. 7, 2016, among 1,012 U.S. investors. Approximately 40% of U.S. adults meet the survey's criteria as investors; these criteria involve having $10,000 or more invested in stocks, bonds or mutual funds, either in an investment or retirement account. Seven in 10 employed investors say their current employer offers a 401(k) -- and of these, 88% say they participate.

Although 401(k) plans offer tremendous opportunity for investors to achieve financial freedom in retirement, the onus for managing them falls on individuals. Along with saving enough, making the right investment decisions at each stage of a worker's career -- which involves maximizing growth while managing risk -- is key to building wealth.

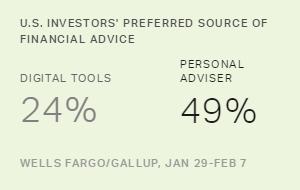

Internet, Personal Adviser Tie as Preferred Source of Advice

Among six tools or resources that investors use to help them allocate their 401(k) investments, Internet research and personal financial advisers tie for the most commonly used -- with 58% of investors naming each. These are followed by online investment calculators, at 46%, and advice from family and friends, at 40%. One in five investors (21%) use target-date funds, which automate allocation based on the date investors plan to start taking withdrawals.

Although 78% of investors who are currently enrolled in a 401(k) say they have access to a financial call center through their plan, only 15% say they rely on it for allocation advice.

Majorities of investors younger than age 50 and those closer to retirement age say they rely on a personal financial adviser. However, it is the top resource used by those aged 50 and older while it ranks second to Internet research among those aged 18 to 49.

| Total% | 18 to 49% | 50+% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| A personal financial adviser | 58 | 52 | 63 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Internet research | 58 | 66 | 49 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Online investment calculators and other financial tools | 46 | 58 | 35 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Advice from family or friends | 40 | 50 | 30 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Target-date funds | 21 | 23 | 18 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Advice through a financial call center | 15 | 10 | 21 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Jan. 29-Feb. 7, 2016 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Wells Fargo/Gallup Investor and Retirement Optimism Index | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Other age-related differences in preference for receiving allocation advice underscore generational gaps in the use of digital versus traditional resources:

-

A majority of investors younger than 50 (58%) versus a third of those aged 50 and older (35%) use online investment calculators.

-

Older investors are twice as likely as those aged 18 to 49 to consult a financial call center (21% vs. 10%, respectively).

-

Younger investors (50%) are also much more likely than older investors (30%) to turn to family or friends for allocation advice.

Bottom Line

According to a 2015 Wells Fargo/Gallup Investor and Retirement Optimism Index survey, roughly two-thirds of employed investors who have a 401(k)-type plan said they can manage it on their own while 35% said they need advice. And when asked which of five areas of investing they need the most help with, the largest percentages mentioned knowing what to invest in (32%) and knowing when to reallocate funds (29%). The latest research clarifies how investors go about answering these important questions.

The majority turn to a personal financial adviser, but many -- particularly younger investors -- also identify Internet research and online investment tools as helpful. Although financial call centers are commonly available, relatively few investors take advantage of them for allocation advice, and those who do tend to be older.

Survey Methods

Results for the Wells Fargo/Gallup Investor and Retirement Optimism Index survey are based on questions asked Jan. 29-Feb. 7, 2016, on the Gallup Daily tracking survey, of a random sample of 1,012 U.S. adults having investable assets of $10,000 or more.

For results based on the total sample of investors, the margin of sampling error is ±4 percentage points at the 95% confidence level. All reported margins of sampling error include computed design effects for weighting.

Each sample of national adults includes a minimum quota of 60% cellphone respondents and 40% landline respondents, with additional minimum quotas by time zone within region. Landline and cellular telephone numbers are selected using random-digit-dial methods.

Learn more about how the Wells Fargo/Gallup Investor and Retirement Optimism Index works.