Story Highlights

- Only 54% optimistic they can maintain income in next year

- 64% optimistic about investment goals over next five years

- 60% say now is not a good time to invest in stocks

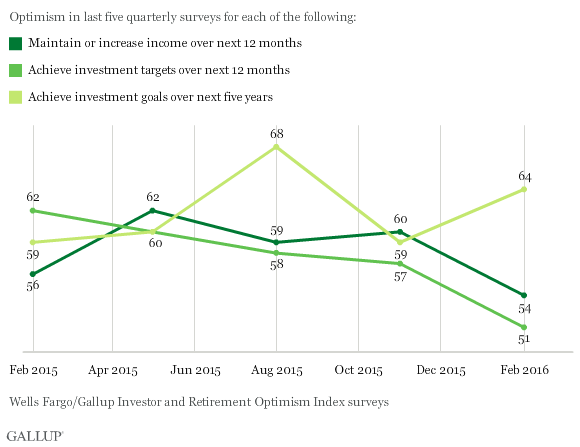

WASHINGTON, D.C. -- A slim majority of retired U.S. investors -- 54% -- are optimistic they can maintain their current income over the next 12 months, and a similar percentage (51%) are optimistic they can meet their investment targets in the next year. Both figures are down from 2015, when closer to 60% in every quarter were optimistic about the two goals.

However, retired U.S. investors are more positive about the longer term than the short term, with 64% now optimistic about meeting their investment goals over the next five years. That is slightly higher than the average in 2015.

In the long run, most (83%) are still confident that their savings will be enough to last throughout their lives. However, tying in with the decline in retirees' optimism about maintaining or growing their income, the percentage who are "very confident" their savings will last has slipped slightly from 47% in the previous survey to 39% now.

Nonretired U.S. investors express similar optimism as retirees about meeting their short- and long-term investment goals, but are significantly more optimistic about maintaining or increasing their income over the next year: 65% vs. 54%.

Market Volatility Taking a Toll on Retired U.S. Investors' Confidence

With stock market volatility spilling over from last year into 2016, retired U.S. investors are more wary of putting their money into stocks. Sixty percent now say it is not a good time to invest in stocks, up from 45% the previous quarter. By contrast, a slight majority of nonretired U.S. investors (52%) still believe it is a good time to invest, while 45% say it is not.

Confidence has also dipped among retired investors in the stock market as a place to save and invest for retirement. Just over one-third (36%) have "quite a lot" (27%) or "a great deal" (9%) of confidence now, compared with 42% in the earlier survey.

Volatility in the stock market remains a concern for about two-thirds (67%) of retired U.S. investors, virtually the same percentage as in the previous survey (66%). However, a majority (54%) believe the recent volatility is a temporary pattern, not the new normal. Matching their actions to that outlook, more than eight in 10 (84%) retired investors made no changes to their stock portfolio during the January market plunge.

The most recent findings are from the 2016 first-quarter Wells Fargo/Gallup Investor and Retirement Optimism Index survey of U.S. investors conducted Jan. 29-Feb. 7 and the 2015 fourth-quarter survey conducted Oct. 30-Nov. 8. For the surveys, investors are defined as U.S. adults who have at least $10,000 invested in stocks, bonds or mutual funds, either in an investment account or a retirement fund -- a definition that approximately 40% of U.S. adults fit.

Optimism Down for Stocks, Steady for Economy, Unemployment

Optimism among retired U.S. investors concerning the national economic picture over the next year is mixed. Slightly less than half are optimistic about economic growth (47%) and unemployment (47%), about four in 10 (42%) are optimistic about inflation, and 37% are optimistic about the stock market. Stock market optimism has declined from 46% in the previous quarter. Optimism has held steady on U.S. economic growth and unemployment.

Bottom Line

Few retired U.S. investors are making changes to their stock portfolio, and a strong majority are still optimistic they will achieve their long-term investment goals. However, it appears that the ups and downs of the stock market have eroded the confidence of some retired investors, raising the question of how much damage future market volatility will do.

Survey Methods

Results for the Wells Fargo/Gallup Investor and Retirement Optimism Index survey are based on questions asked Jan. 29-Feb. 7 on the Gallup Daily tracking survey, of a random sample of 316 U.S. retirees and 694 nonretirees having investable assets of $10,000 or more.

For results based on the total sample of retirees, the margin of sampling error is ±6 percentage points for retired investors and ±5 percentage points for nonretired investors at the 95% confidence level. All reported margins of sampling error include computed design effects for weighting.

Each sample of national adults includes a minimum quota of 60% cellphone respondents and 40% landline respondents, with additional minimum quotas by time zone within region. Landline and cellular telephone numbers are selected using random-digit-dial methods.

Learn more about how the Wells Fargo/Gallup Investor and Retirement Optimism Index works.