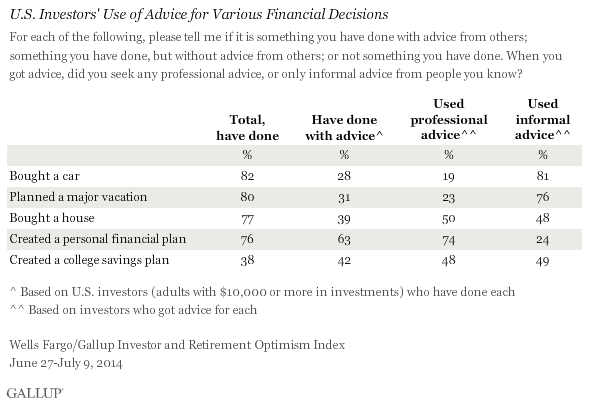

PRINCETON, NJ -- U.S. investors have made a number of important financial decisions in their lives, but their propensity to seek advice, and particularly professional advice, varies widely depending on the activity. Purchasing a car is the most common financial decision of five tested, but it is the one investors are the least likely to say they have done with any sort of advice. Investors are most likely to have sought advice when creating a personal financial plan, with 63% doing so, and three-quarters of these saying it was professional, as opposed to informal, advice.

These findings are based on the Wells Fargo/Gallup Investor and Retirement Optimism Index survey conducted June 27-July 9, 2014. The survey is based on a nationally representative sample of U.S. investors with $10,000 or more in stocks, bonds, mutual funds, or self-directed IRAs or 401(k) accounts.

Roughly four in five investors have experience with most of the activities asked about in the poll. This includes 82% buying a car, 80% planning a major vacation, 77% purchasing a house, and 76% creating a personal financial plan. The only activity that is significantly less common is creating a college savings plan -- something 38% of investors say they have done.

Of those who have experience with each financial decision or activity, the percentage who have sought some sort of advice in the process ranges from 63% for creating a personal financial plan to 28% for buying a car. Close to half of investors have sought advice for creating a college savings plan, about three in 10 have sought advice for planning a major vacation, and 39% have done so for buying a house. While few investors -- 38% -- say they have ever created a college savings plan, a relatively large proportion of those who have -- 42% -- say they sought advice when doing so.

Separately, the poll finds a wide range of reliance on professional advice among those who have sought any type of advice for each activity. As noted, three-quarters of those who have sought advice for a personal financial plan used professional advice, as opposed to informal advice from people they know. About half of advice-seekers for buying a house and creating a college savings plan used professional advice. But the percentage goes way down for those planning a major vacation -- less than a quarter (23%) of those who have sought advice sought it from a professional -- as well as for buying a car (19%).

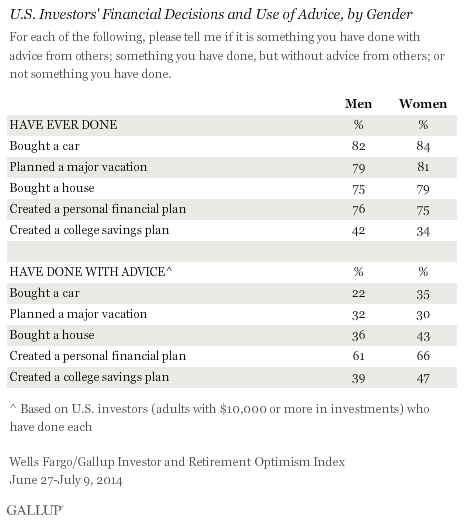

Women More Likely Than Men to Ask for Help

While men and women report similar levels of experience with most of the activities, women are more likely to say they have sought advice for three of them. The gap is especially large for purchasing a car: 22% of men versus 35% of women have sought advice when buying one. Women are also more likely than men to have sought advice when buying a house and creating a college savings plan. However, among advice-seekers, there is no difference in men's and women's likelihood of getting professional advice versus informal advice from people they know.

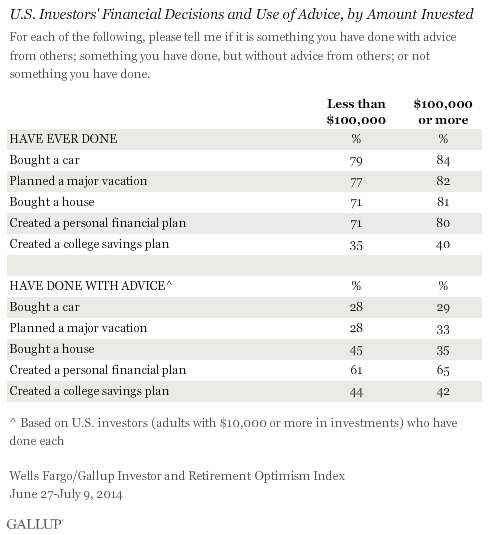

The poll also finds that investors with $100,000 or more in investable assets are slightly more likely than those with less than $100,000 to have experience with each type of financial decision. However, the two groups are relatively similar in reporting that they sought advice for each. The only exception is that investors with less than $100,000 in investments are more likely than those with greater investments to say they have sought advice when buying a house: 45% vs. 35%.

Bottom Line

Even if it costs something, seeking professional advice for major financial decisions can be a great strategy if the advice saves or makes one money in the long run. But more often than not, U.S. investors seek advice informally from friends and family, or get no advice.

The one major exception to this is when creating a personal financial plan. Three-quarters of investors (76%) report having created a personal financial plan at some point. Of those who did, 63% say they sought advice from others -- and among those who sought advice, roughly three-quarters (74%) say they sought professional advice. This is much higher than the percentage of advice-seekers who sought professional advice when buying a car (19%), planning a major vacation (23%), buying a house (50%), or even creating a college savings plan (48%).

Higher proportions of investors have made some of these other major financial decisions than have created a financial plan, but none of these decisions is nearly as likely to compel investors to seek professional advice. Whether this is because of the perceived complexity of planning out one's finances, because of the importance of it, or because of the amount of money involved isn't clear.

Survey Methods

These findings are part of the Wells Fargo/Gallup Investor and Retirement Optimism Index survey, conducted June 27-July 9, 2014, by telephone. The sample included 1,036 investors, aged 18 and older, living in all 50 states and the District of Columbia. For this study, the American investor is defined as any person or spouse in a household with total savings and investments of $10,000 or more. About two in five American households have at least $10,000 in savings and investments in stocks, bonds, mutual funds, or self-directed IRAs or 401(k) accounts. The sample consists of 72% nonretired investors and 28% retired investors.

Questions about investors' use of professional advice were asked of a random half-sample of 509 U.S. investors. The margin of sampling error for these results is ±5 percentage points at the 95% confidence level.

Interviews are conducted with respondents on landline telephones and cellular phones, with interviews conducted in Spanish for respondents who are primarily Spanish-speaking. Each sample of national adults includes a minimum quota of 50% cellphone respondents and 50% landline respondents, with additional minimum quotas by time zone within region. Landline and cellular telephone numbers are selected using random-digit-dial methods. Landline respondents are chosen at random within each household on the basis of which member had the most recent birthday.

Samples are weighted to correct for unequal selection probability, nonresponse, and double coverage of landline and cell users in the two sampling frames. They are also weighted to match the national demographics of gender, age, race, Hispanic ethnicity, education, region, population density, and phone status (cellphone only/landline only/both, and cellphone mostly). Demographic weighting targets are based on the most recent Current Population Survey figures for the aged 18 and older U.S. population. Phone status targets are based on the most recent National Health Interview Survey. Population density targets are based on the most recent U.S. census. All reported margins of sampling error include the computed design effects for weighting.

In addition to sampling error, question wording and practical difficulties in conducting surveys can introduce error or bias into the findings of public opinion polls.

For more details on Gallup's polling methodology, visit www.gallup.com.