Story Highlights

- In first decade, half depend on other employer for insurance

- Health insurance source changes with age, employment status

- Finding good employees more difficult without health benefits

WASHINGTON, D.C. -- While the vast majority of microbusiness owners have health insurance, only 31% provide it for themselves through their own business or out of pocket, according to the Sam's Club/Gallup Microbusiness Tracker. Just as many have insurance through a former or current employer that is not their business, while another 19% depend on Medicare instead. Providing for at least the owner's health insurance appears to mark an important milestone as these smallest of businesses develop over time.

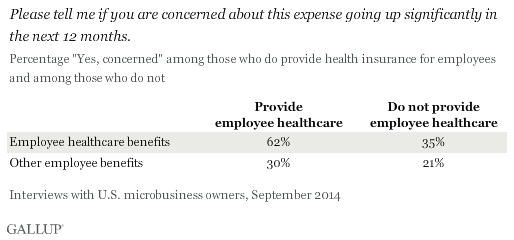

Offering employee health benefits is costly for most in the U.S. Microbusinesses, defined as having five or fewer workers, are too small to take advantage of significant economies of scale when negotiating insurance premiums and so generally pay much more per employee for their insurance packages than larger businesses do. Only one in five (21%) microbusiness owners who have at least one employee say they provide health insurance for their employees. That may in part be explained by the substantial 41% of employer microbusiness owners who say they are concerned about a significant increase in the cost of providing health benefits in the next 12 months. Owners who do provide healthcare are understandably much more likely to be concerned about these costs and to count this as a major issue facing their businesses.

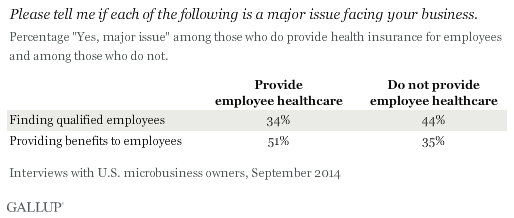

Though microbusinesses are not large enough to be legally required to provide employee health insurance, attracting and recruiting talented employees can be much more difficult without this important benefit. Indeed, microbusiness owners who provide employee health coverage are less likely than those who don't to say that finding qualified employees is a major issue.

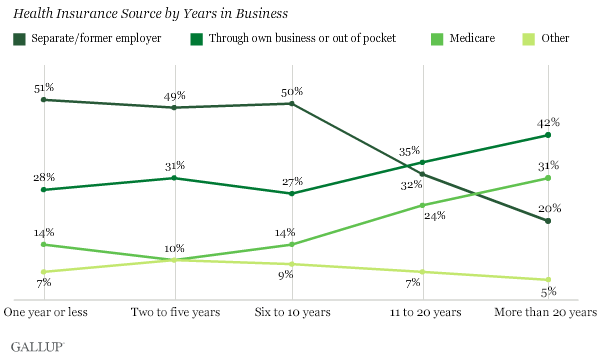

Health Insurance Source Changes With Age, Employment Status

The Sam's Club/Gallup Microbusiness Tracker reported in early 2014 that many microbusiness owners maintain a second job outside their business, with almost one-third (31%) getting more personal income from that job than from their business. By the same token, about half of microbusiness owners who have been in business for a decade or less depend on a separate/former employer's insurance, while only about one-third provide it themselves. But owners who have been in business more than 10 years -- and in particular those in business for more than 20 years -- are more likely to provide their own health insurance than to depend on a separate employer. The percentage getting their health insurance from Medicare also increases among those in business longer -- though this is not surprising, given that many owners who have been in business that long are 65 or older, and thus eligible for Medicare coverage.

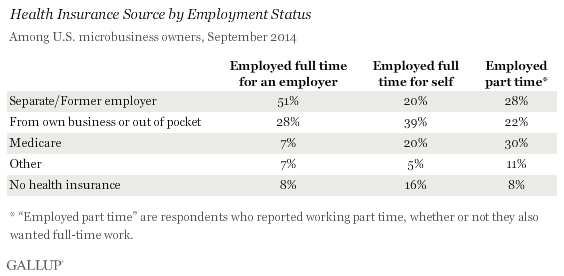

Microbusiness owners who get their health insurance through their business overwhelmingly identify as being employed full time (86%), either for an employer or for themselves. Most (69%) are 50 to 64 years of age and employ others at their business (72%). Those who identify as "employed full time for an employer" are most likely to get their insurance from a job other than the business they own. They are about equally likely to get most of their income from such a job as to get it from their business. Owners who say they are full-time "self-employed" are the most likely to pay for their own insurance through their business or out of pocket (39%, vs. 31% for all microbusiness owners).

Bottom Line

Most Americans depend on their employer for health insurance coverage, and providing health insurance to employees -- including oneself -- is a major business cost that has been growing for decades. Health insurance coverage is expensive for most in the U.S., but per-person costs can be brought down significantly with the group insurance plans that most large employers negotiate. However, microbusinesses have the least financial and organizational resources of any business to begin with, and can't benefit from the economies of scale of larger businesses' health plans.

Microbusinesses must often compete with larger businesses for the same pool of employee candidates, with a significant handicap in the employee benefits they can offer. On average, microbusiness owners who have been in business longer are more likely to say they provide this benefit, though it is still much less than a majority. However, owners who provide health benefits are less likely to say finding qualified employees is an issue, suggesting that offering health insurance is a real advantage when hiring. Perhaps more than any other metric, covering at least the owner's health coverage appears to be an important milestone for these smallest of businesses in becoming self-sufficient enterprises with the ability to grow.

Survey Methods

Results for the Sam's Club/Gallup Microbusiness Tracker are based on telephone interviews conducted on a quarterly basis with a random sample of microbusiness owners aged 18 and older, living in all 50 U.S. states and the District of Columbia. Business owners selected were those who reported owning a "microbusiness" with five or fewer workers, including the owner. Results from the Quarter 3, 2014, study are based on 1,005 interviews conducted Sept. 2-16, 2014. For results based on the total sample of Quarter 3, 2014, business owners, the margin of sampling error is ±4.2 percentage points at the 95% confidence interval.

Interviews were conducted with respondents on landline and cellular telephones. All interviews were conducted in English. Respondents were chosen at random from a group of people who had completed a previous general Gallup telephone interview and indicated they were a business owner and were willing to be contacted for a future survey. The sample was stratified by businesses size and weighted for business size and region.

Learn more about how the Sam's Club/Gallup Microbusiness Tracker works.