Story Highlights

- Nonretirees more likely to say it's "critical" than retirees

- Three in four investors have some form of debt

- Seven in 10 say certain amount of debt is necessary, acceptable

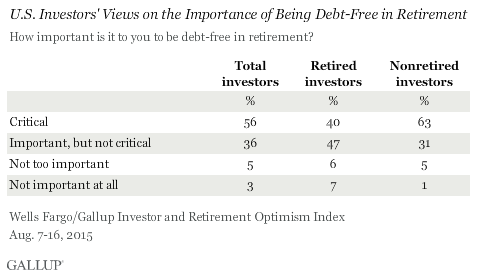

WASHINGTON, D.C. -- More than half of U.S. investors say it is "critical" to be debt-free in retirement, while another third say it is "important, but not critical." Notably, investors who have not retired yet are much more likely than retirees to say being out of debt is critical.

These findings are from the third-quarter Wells Fargo/Gallup Investor and Retirement Optimism Index survey, conducted Aug. 7-16. Investors are defined for this survey as U.S. adults who have at least $10,000 invested in stocks, bonds or mutual funds, a criterion met by 44% of U.S. adults in the current survey.

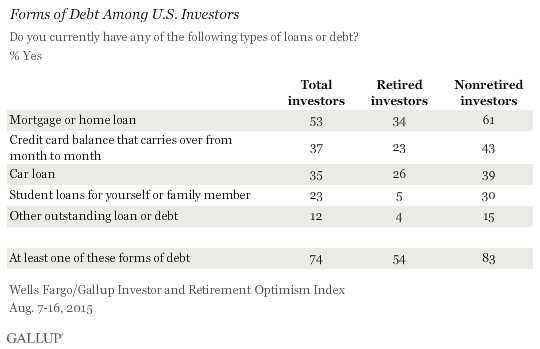

Three in four investors have some type of debt, whether that be a mortgage (53%), credit card balance (37%), car loan (35%), student loan (23%) or some other type of debt (12%). The rates are significantly higher for nonretirees than retirees, leading to 83% of all nonretirees having at least one type of loan, compared with 54% of retirees.

While nonretired investors may be optimistic about achieving debt freedom in retirement, resulting in the large proportion who say achieving that status will be critical, retirees are much more realistic about it. Only 22% of retired investors with debt say being debt-free in retirement is critical, helping to explain the lower "critical" response among retired investors overall. By contrast, 60% of retired investors with no debt say being debt-free in retirement is critical to them.

Half of Investors With Debt Say They Have Made a "Major Effort" to Reduce It

Investors are far from cavalier about their debt. Of those with one or more types of loans or credit card balances, half say they have made a "major effort" to reduce their debt in the coming years, and even more intend to make a "major effort" to reduce it going forward (62%).

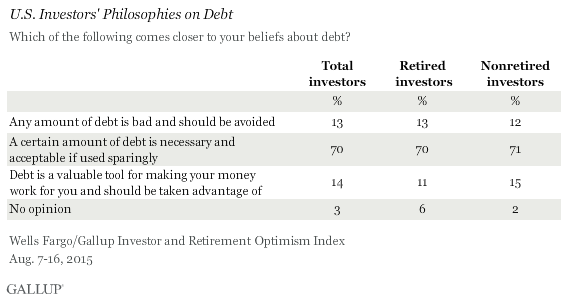

Investors take a moderate stand on the prudence of debt, with 70% saying a certain amount is necessary and acceptable. Just 13% embrace the philosophy espoused by some prominent financial experts, such as author and radio host Dave Ramsey, that any amount of debt should be avoided, while an equal proportion (14%) take the opposite view that debt is a powerful tool for growing wealth and should be taken advantage of.

Bottom Line

Investors rely on debt to accomplish a variety of life goals, such as homeownership, paying for college and purchasing a car. While the large majority of nonretired investors put a high value on being debt-free in retirement, retired investors -- about half of whom carry debt -- are less likely to see that as highly important. Retired investors' views are largely influenced by their own situation in retirement, while nonretired investors may be answering from a normative perspective about what they would like their financial situation to be (but may not end up actually being the reality) when they retire.

In any case, American investors take their debt very seriously. The large majority of them are making at least some effort to reduce it now and going forward. This isn't to say that investors see debt as a bad thing -- seven in 10 say debt is necessary and acceptable to use sparingly. Just one in eight see all debt as bad, while a similarly sized minority say debt is a valuable tool to leverage.

Survey Methods

Results for the Wells Fargo/Gallup Investor and Retirement Optimism Index survey are based on questions asked Aug. 7-16, 2015, on the Gallup Daily tracking survey, of a random sample of 482 U.S. adults having investable assets of $10,000 or more, including 330 who have any amount of debt.

For results based on the entire sample of investors, the margin of sampling error is ±4 percentage points at the 95% confidence level.

In addition to sampling error, question wording and practical difficulties in conducting surveys can introduce error or bias into the findings of public opinion polls.

Learn more about how the Wells Fargo/Gallup Investor and Retirement Optimism Index works.