Story Highlights

- 48% expect to live comfortably in retirement

- 74% of U.S. retirees say they are living comfortably

- Many affluent Americans expect to take a retirement hit

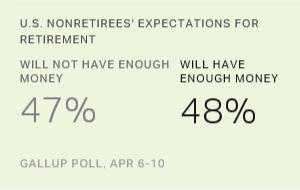

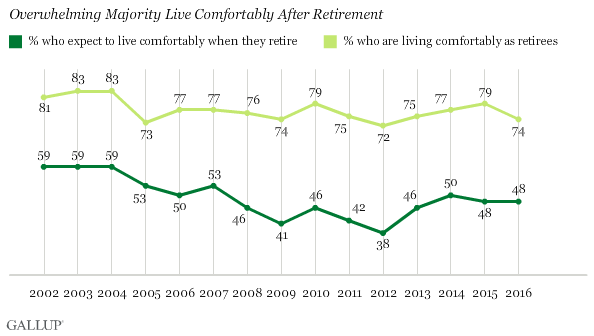

WASHINGTON, D.C. -- Almost half of Americans (47%) who are not retired think that when they do retire, they won't have enough money to live comfortably. And about the same number (48%) expect they will have enough. Those who have already made the move to retirement, however, tell a different story: 74% say they have enough money to live comfortably.

The gap between the percentage of U.S. nonretirees who think they will live comfortably once they retire and the percentage of retirees who actually are living comfortably is not a new phenomenon; it has existed since Gallup first asked both questions in 2002. The gap was widest in the economically tumultuous years from 2008 to 2012 -- a period when plummeting property and stock values caused many still in the workforce to grow pessimistic about their long-term financial prospects.

The combination of falling house prices and the financial crisis affected some of the key income sources many Americans count on for retirement. In an April 2007 Gallup poll, 24% listed stocks as an expected major source when they retired; 30% listed equity in their homes; and 52% named 401(k), individual retirement account (IRA), Keogh or other retirement savings accounts. As each of these potential sources shrank in value for many Americans, optimism about living comfortably in retirement fell from 53% in 2007 to 41% in 2009 and bottomed out in 2012 at 38%.

Among those closest to retirement during the 2008-2012 period, those aged 50 to 64, only 35% said they expected to retire to a comfortable lifestyle. The percentage has not risen much among those aged 50 to 64 in the past four years, averaging 41%.

However, in combined polls from 2014 to 2016, three in four (75%) younger retirees -- those aged 61 to 70 and therefore most likely to have retired since 2008 -- say they are living comfortably. The percentage is only a few points lower than the 79% of older retirees who say they are living comfortably. These findings suggest that fears of being short of money among those looking retirement directly in the face are generally not borne out once they actually retire.

Largest Gap Occurs Among Most Affluent, Those Closest to Retirement

Combining the data from the three 2014-2016 Gallup Economy and Personal Finance polls allows a look at how income and age potentially affect optimism about living comfortably in retirement.

-

Among younger adults, attitudes about current living situations come close to matching what they expect when they retire in the distant future. But at all other age levels, there is a pronounced gap. Sixty-three percent of those younger than age 30 say they are living comfortably now, and 58% expect to live comfortably when retired. The percentage expecting a comfortable retirement drops significantly among nonretirees aged 30 and older, while the percentage currently living comfortably stays at about the same level or increases. Among those between the ages of 60 and 69 who have not yet retired, 68% say they are living comfortably, but 50% expect that to continue when they retire.

-

Nearly one in three (32%) nonretirees with annual household incomes below $30,000 say they are living comfortably now, and the same percentage expect to live comfortably in retirement. A clear divide emerges between the two measures as income increases, and among those earning $75,000 or more, 90% say they are currently living comfortably, but only 64% expect to live comfortably once retired. Those in the $75,000-and-above bracket are twice as likely to think they will live comfortably in retirement as those who earn less than $30,000, but they are also far more likely to expect that they will lose their comfortable lifestyle when they retire.

| Living comfortably now% | Expect to live comfortably in retirement% | Differencepct. pts. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Age | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 18-29 | 63 | 58 | 5 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 30-39 | 65 | 46 | 19 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 40-49 | 70 | 46 | 24 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 50-59 | 60 | 42 | 18 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 60-69 | 68 | 50 | 18 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Annual Income | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Less than $30,000 | 32 | 32 | 0 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $30,000-$49,999 | 59 | 43 | 16 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $50,000-$74,999 | 70 | 47 | 23 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $75,000 and above | 90 | 64 | 26 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2014, 2015 and 2016 Gallup polls of 1,034 nonretirees | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Bottom Line

Americans have had concerns about the affordability of retirement for decades. A 1989 Gallup poll found that 74% of workers aged 30 or older worried they would not have enough money to live comfortably when they retired. More recently, workers have been given plenty of reasons to worry. The housing market collapse of 2007-2012 eroded the value of homes, and the financial crisis in 2008 made major inroads on savings heavily invested in the market. Politicians and pundits have sounded warnings about the solvency of Social Security, and articles describing long-term financial dangers facing retirees have proliferated.

This atmosphere has created retirement worries that reach far beyond those Americans facing serious financial difficulties. In Gallup's three most recent polls, 25% of nonretirees earning $100,000 or more annually do not expect to live comfortably when they retire. In those same three polls, more than half (58%) of nonretirees who are living comfortably now worry about having enough money for retirement. Even among those who are retired and living comfortably, 31% worry that it won't last.

The experience of recent retirees, most of whom report that they are living comfortably, provides some evidence that fears of retirement woes have been overblown. But complicating factors -- including people living longer, the drying up of pension funds and the low levels of savings among Americans in recent years -- seem to guarantee that no clear answers will be known for years to come.

Survey Methods

Results for this Gallup poll are based on telephone interviews conducted April 6-10, 2016, with a random sample of 1,015 adults, aged 18 and older, living in all 50 U.S. states and the District of Columbia. For results based on the total sample of national adults, the margin of sampling error is ±4 percentage points at the 95% confidence level.

Each sample of national adults includes a minimum quota of 60% cellphone respondents and 40% landline respondents, with additional minimum quotas by time zone within region. Landline and cellular telephone numbers are selected using random-digit-dial methods.

Learn more about how the Gallup Poll Social Series works.