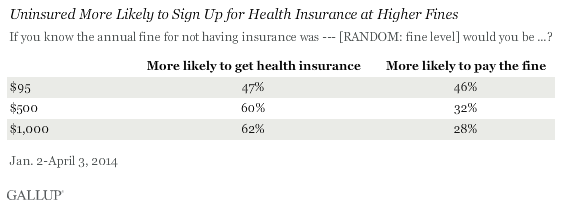

WASHINGTON, D.C. -- Uninsured Americans' likelihood of signing up for insurance differs depending on the amount of the fine they would have to pay for not carrying insurance. At a hypothetical $95 fine level, uninsured Americans are as likely to say they would not get insurance (46%) as to say they would (47%). At a $500 fine level, the percentage saying they would get insurance jumps to 60%, but this percentage levels off at a $1,000 fine level at 62%.

The results are based on interviews with 4,829 Americans without health insurance as part of Gallup Daily tracking from Jan. 2-April 3, 2014. Uninsured Americans were randomly assigned to three groups, each testing respondents' likelihood to sign up for insurance under different fine conditions of $95, $500, and $1,000.

Under the Affordable Care Act, also commonly known as "Obamacare," U.S. adults and their dependents must have health insurance or pay a fine. In 2014, the fine is $95 or 1% of household income, whichever is greater. The fine increases to $325, or 2% of taxable income, in 2015 and $695, or 2.5% of income, in 2016. These Gallup Daily tracking results provide a broad indication of how consumers would react to the three thresholds of fines.

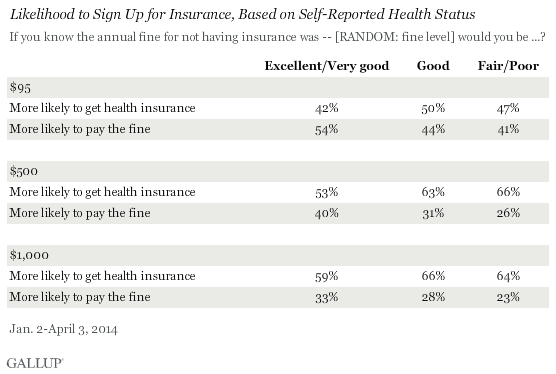

Healthy Less Likely Than Sick to Sign Up, Regardless of Fine Amount

Health insurance companies and stakeholders believe the most important factor in the future pricing and overall affordability of health insurance plans could be uninsured healthy individuals signing up for insurance at similar rates to less healthy uninsured individuals. With this concept in mind, Gallup asked respondents to self-report their health as "excellent," "very good," "good," "fair," or "poor." This measurement has proven to correlate with self-reporting of chronic and expensive health conditions like obesity, high blood pressure, and depression.

Across the various fine levels, adults with excellent or very good self-reported health are less likely to say they would sign up for health insurance than adults with poorer health. However, increasing the fine does increase the likelihood that healthier adults will enroll in a plan. At the $1,000 level, a solid majority of Americans in all health groups measured report being more likely to sign up for insurance than paying the fine.

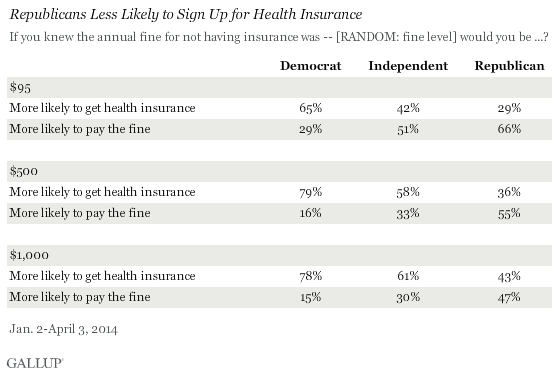

Fine Levels Affect Democrats and Republicans Equally

The data show that respondents' political affiliation plays a role in their stated likelihood of signing up for health insurance. At each fine level, those who identify as Republican are about half as likely to report a willingness to sign up for health insurance as those who identify as Democrat.

These political affiliation findings are consistent with earlier Gallup reports on how party identification affects Americans' attitudes toward the Affordable Care Act and uninsured Americans' intentions to get insurance.

Implications

The increase in the Affordable Care Act fine next year to a minimum $325, or 2% of one's yearly household income, could compel a significant amount of still-uninsured Americans who did not sign up during the open enrollment period to do so in 2015. This increase could begin to taper off between the 2015 and 2016 tax years if the average fine moves between $500 and $1,000. At this point, there is a distinct possibility that the growth in the insurance coverage rate will either slow down or stall based on expected future fine levels. However, other factors such as public support for the Affordable Care Act and targeted marketing campaigns may help to close the insurance coverage gap even as the fines lose some of their ability to influence decision making.

Survey Methods

Results for this Gallup poll are based on telephone interviews conducted between Jan. 2-April 3, 2014, on the Gallup Daily tracking survey, with a random sample of 4,929 adults, aged 18 and older, living in all 50 U.S. states and the District of Columbia, who do not currently have health insurance.

Each experimental fine level ($95, $500, or $1,000) was asked of a randomly selected third of the overall sample, approximately 1,600 uninsured Americans per condition. For results based on these samples of uninsured Americans, the margin of sampling error is ±3 percentage points at the 95% confidence level.

Interviews are conducted with respondents on landline telephones and cellular phones, with interviews conducted in Spanish for respondents who are primarily Spanish-speaking. Each sample of national adults includes a minimum quota of 50% cellphone respondents and 50% landline respondents, with additional minimum quotas by time zone within region. Landline and cellular telephone numbers are selected using random-digit-dial methods. Landline respondents are chosen at random within each household on the basis of which member had the most recent birthday.

Samples are weighted to correct for unequal selection probability, nonresponse, and double coverage of landline and cell users in the two sampling frames. They are also weighted to match the national demographics of gender, age, race, Hispanic ethnicity, education, region, population density, and phone status (cellphone only/landline only/both, and cellphone mostly). Demographic weighting targets are based on the most recent Current Population Survey figures for the aged 18 and older U.S. population. Phone status targets are based on the most recent National Health Interview Survey. Population density targets are based on the most recent U.S. census. All reported margins of sampling error include the computed design effects for weighting.

In addition to sampling error, question wording and practical difficulties in conducting surveys can introduce error or bias into the findings of public opinion polls.

For more details on Gallup's polling methodology, visit www.gallup.com.