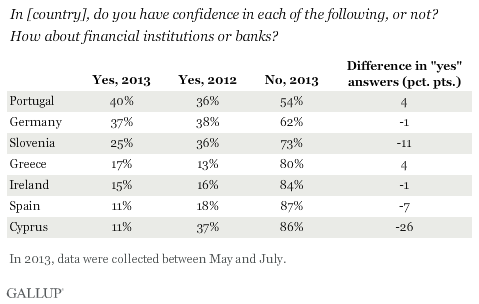

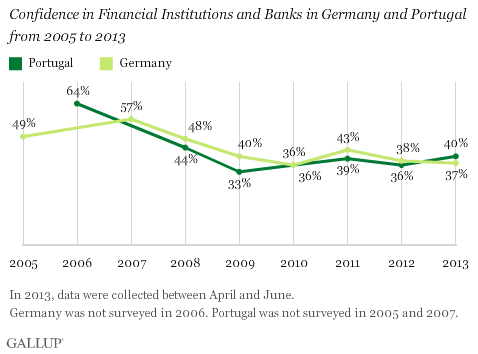

WASHINGTON, D.C. -- Portuguese confidence in their country's banking and financial institutions has remained relatively intact compared with attitudes in other eurozone countries that received bailouts. While trust in banks continues to erode in Cyprus and Spain, trust in Portugal remains stable, at 40%, and on par with bailout funder Germany.

Although Portuguese interviewed from May through June this year express a relatively higher level of trust in their banks, a majority (54%) do not have confidence. Residents of Greece, Ireland, Spain, and Cyprus are much less likely to be confident in the banks in their respective countries, with at least eight in 10 lacking trust.

Portugal's crisis, unlike the crises in Ireland, Spain, and Cyprus, was not primarily a banking crisis, but a sovereign debt crisis, which may partly explain the relatively higher Portuguese confidence in financial institutions. Yet, several Portuguese banks did receive funds from the country's 78 billion euro bailout package requested in the first half of 2011. The 3 billion euro rescue in June 2012 of Millennium bcp, Portugal's largest listed bank by assets, does not appear to have had any detrimental effect on Portuguese residents' trust in their banks.

While Germans' trust in their banks has also remained virtually unchanged this year compared with last year, it has not recovered to levels found before the banking crisis. This is despite the German economy's impressive rebound after the global financial and economic crisis. Some 646 billion euros was spent or set aside to rescue German banks from 2008 through 2012, according to figures from the European Commission. Since 2007, Germans' trust in the country's financial institutions has fallen by 20 percentage points.

Confidence in Banks Falls to All-Time Lows in Cyprus, Spain, and Slovenia

The huge 26-point slump in Cypriots' trust in their financial institutions and banks between April-May 2012 and May 2013 is hardly surprising given that Cyprus became the fifth country to receive rescue loans from the EU and the International Monetary Fund (IMF) in March 2013. This was the first such bailout deal that forced losses on deposit holders. Similarly, Spaniards' trust in their banks also sank to an all-time low of 11% in May 2013 after the Rajoy administration requested European funds to recapitalize its struggling banks in late 2012.

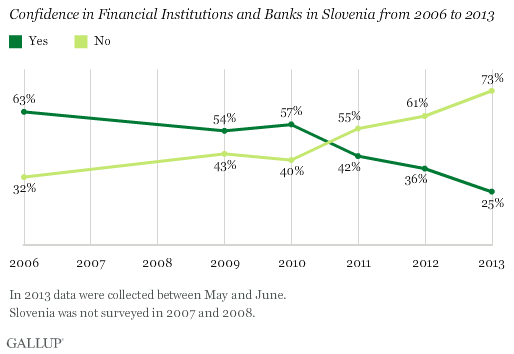

In addition, in Slovenia, which many experts believe could be the next eurozone country to need a bailout, 25% of residents express confidence in its banks, down from 36% in 2012. Surveys in Slovenia took place May-June 2013, three months before the Slovenian government provided guarantees for two small troubled banks -- a development that might have undermined Slovenes' trust in their banks even more.

Slovenia joined the eurozone in 2007 and was its fastest growing member at that time. The country's economy suffered immensely from the global crisis because of its high dependency on exports. At the onset of the economic crisis in 2009, a slight majority (54%) of Slovenes expressed trust in the country's financial institutions and banks. Yet in 2011, this trust started to drop precipitously.

Implications

The continuing, comparatively high level of confidence in financial institutions in Portugal is good news, in addition to the country officially emerging from its recession. In contrast, the case of Slovenia shows that the eurozone crisis is far from over. Slovenes' confidence in their financial institutions and banks has dropped dramatically since 2011 to levels seen in Spain and Greece just before their governments asked EU partners and the IMF for financial help.

In 2012, Europeans were the least likely in the world to trust their banks. Continuing low levels of trust in banks in Spain, Greece, Ireland, and Cyprus may warrant that European governments take more decisive action. If German parliamentarians can agree on a government coalition after the elections that took place on Sept. 22, Germany might finally agree to conclude an agreement on the European banking union. As Gallup's data from Germany reveal, however, reviving economic growth alone does not necessarily restore residents' trust in banks. Tougher scrutiny of banks by European institutions will likely need to be part of the solution.

For complete data sets or custom research from the more than 150 countries Gallup continually surveys, please contact us.

Survey Methods

Results are based on telephone and face-to-face interviews with approximately 1,000 adults, aged 15 and older, per country per year. In Cyprus, excluding the Turkish-controlled areas in the north, 500 interviews per year were conducted. The 2013 data from Germany is based on 750 phone interviews. The 2013 data were collected during the following periods:

- Germany: April 30-June 26, 2013

- Ireland: May 1-June 1, 2013

- Portugal: May 6-June 18, 2013

- Spain: May 7-May 24, 2013

- Slovenia: May 8-June 11, 2013

- Cyprus: May 9-May 28, 2013

- Greece: June 19-July 31, 2013

For results based on the total sample of national adults, one can say with 95% confidence that the maximum margin of sampling error ranges from a low of ±3.5 percentage points to a high of ±5.3 percentage points. The margin of error reflects the influence of data weighting. In addition to sampling error, question wording and practical difficulties in conducting surveys can introduce error or bias into the findings of public opinion polls.

For more complete methodology and specific survey dates, please review Gallup's Country Data Set details.