Story Highlights

- Five-point gap in financial literacy between men and women

- U.S. ranks 14th in literacy worldwide

WASHINGTON, D.C. -- Two-thirds of adults worldwide are financially illiterate, with sizable gaps between men's and women's financial literacy.

These data are from Standard & Poor's Ratings Services Global Financial Literacy Survey of more than 150,000 adults in 148 countries in 2014. Adults were tested on their knowledge of four basic financial concepts: risk diversification, inflation, numeracy and compound interest. Respondents were considered financially literate if they were able to correctly answer questions about three of the four concepts.

Data were collected via the Gallup World Poll, and researchers from the World Bank Development Research Group and the Global Financial Literacy Excellence Center at George Washington University conducted the analysis. The findings represent the world's largest, most comprehensive global measurement of financial literacy to date.

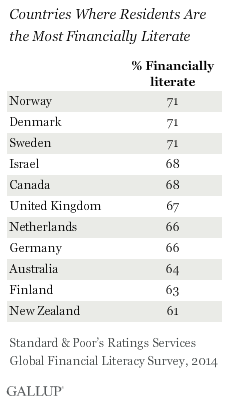

Scandinavian countries have the highest financial literacy rates globally, with Norway, Denmark and Sweden at 71% each. Israel (68%), Canada (68%), the United Kingdom (67%), the Netherlands (66%) and Germany (66%) are also among the most financially literate countries in the world.

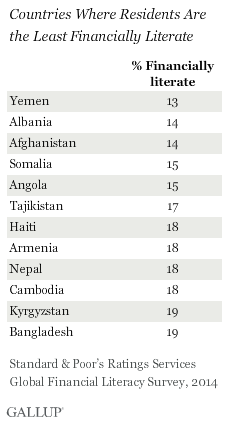

Yemen (13%), Albania (14%) and Afghanistan (14%) are the least financially literate populations worldwide, with one in seven or fewer residents financially literate.

Among the world's largest economies with democratic systems of government, also known as the G7, Italy had the lowest financial literacy rate (37%), while Canadians were the most literate (68%).

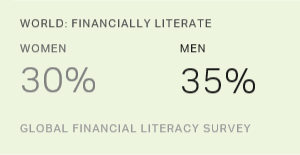

Globally, there is a five-percentage-point gender gap in financial literacy: 35% of men are financially literate, compared with 30% of women. Gender gaps are present in most countries, even in highly developed ones. The gender gap is pronounced in the U.S., for example, where men's financial literacy is 10 points higher than American women's. In addition to these divides, the U.S. also suffers from large financial literacy gaps by income and education.

Fifty-seven percent of U.S. adults overall are financially literate, with the U.S. ranking 14th in the world in financial literacy. U.S. adults have a relatively weak understanding of compound interest, the survey found. Even among those who have a credit card or who finance their homes, one-third of respondents could not correctly answer the compound interest questions.

Bottom Line

Standard & Poor's Ratings Services Global Financial Literacy Survey offers an unprecedented, comprehensive assessment of worldwide financial literacy. This study quantifies financial literacy in more than 99% of the world's adult population, and across geographic and demographic groups. The full report can be found here.

There is a great range of financial literacy worldwide. Even in regions where the most residents are financially literate, there are still sizable financially illiterate populations -- of roughly three in 10 people in several Scandinavian countries, for example.

But while literacy rates may vary from country to country, the disparity between men and women is common worldwide, existing in highly developed and less developed countries alike.

Survey Methods

Data were collected by Gallup as a part of the World Poll. Interviewing was conducted in 2014 in 148 countries. More than 150,000 interviews were conducted. Country samples were probability based and nationally representative of the resident population aged 15 and older. The typical sample size was 1,000 interviews, with higher sample sizes in Russia (2,000), India (3,000) and China (4,184); and smaller sample sizes in Belize, Haiti, Jamaica and Puerto Rico (approximately 500 each).

For results based on the sample of national adults at the country level, the margin of sampling error ranged from ±2.7 percentage points to ±5.2 percentage points at the 95% confidence level. Margins of error for subgroups (such as gender) are higher. All reported margins of sampling error include computed design effects for weighting.

For more complete methodology and specific survey dates, please review Gallup's Country Dataset details.

The following five questions were used to measure financial literacy. Respondents were considered "financially literate" if they answered questions on three of the four topics correctly. Answers to questions about the compound interest topic were considered "correct" if either item was answered correctly.

Risk Diversification

- Suppose you have some money. Is it safer to put your money into one business or investment, or to put your money into multiple businesses or investments?

Inflation

- Suppose over the next 10 years the prices of the things you buy double. If your income ALSO doubles, will you be able to buy less than you can buy today, the same as you can buy today OR more than you can buy today?

Numeracy

- Suppose you need to borrow 100 (country currency). Which is the lower amount to pay back: 105 (country currency) or 100 (country currency) plus 3%?

Compound Interest

- Suppose you put money in the bank for two years and the bank agrees to add 15% per year to your account. Will the bank add MORE money to your account the second year than it did the first year, or will it add the SAME amount of money both years?

- Suppose you had 100 (country currency) in a savings account and the bank adds 10% per year to the account. How much money would you have in the account after five years if you did not remove any money from the account: more than 150 (country currency), exactly 150 (country currency) or less than 150 (country currency)?