The following is based on the recently released 2017 Global Findex report.

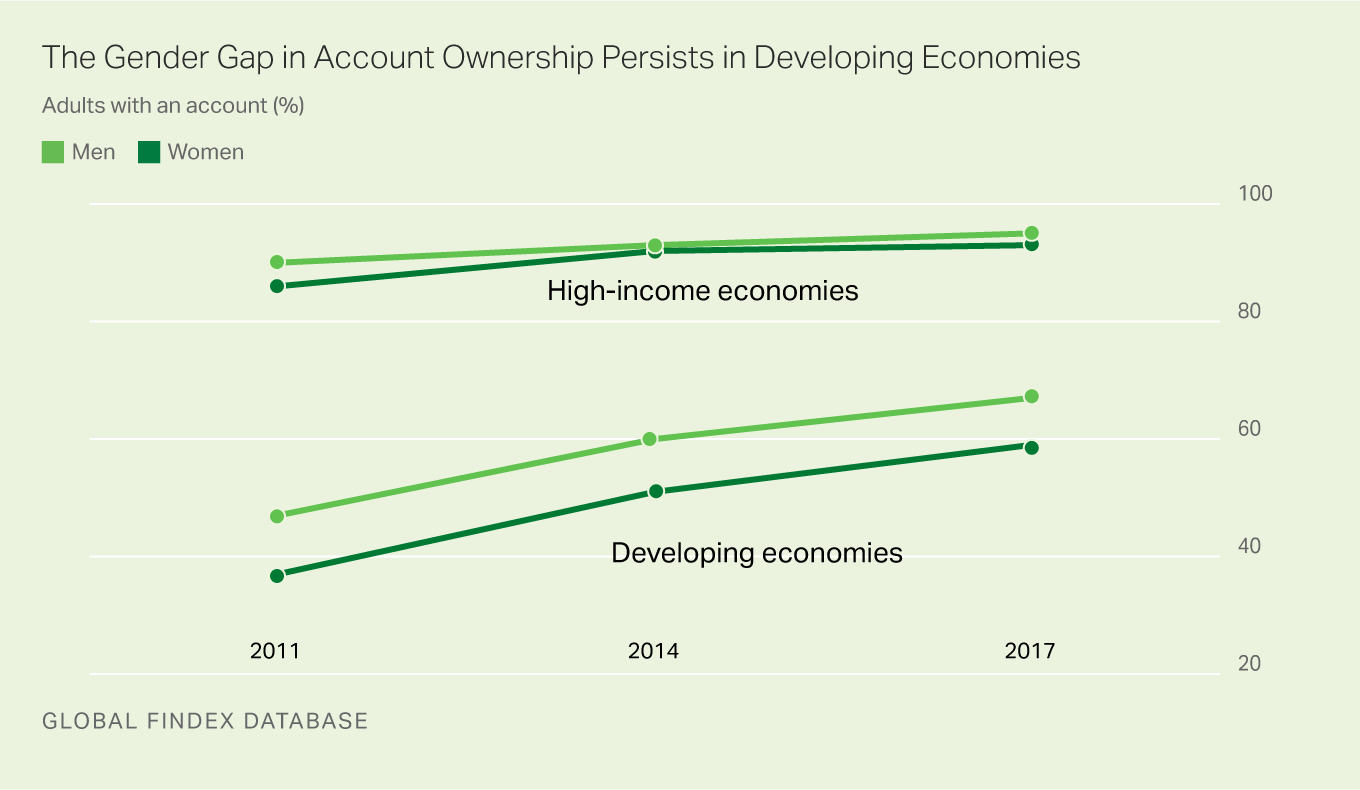

Even as the number of adults worldwide who have bank accounts continues to swell, the latest World Bank Global Findex report shows the gap between men and women remains just as wide as when it was first measured seven years ago.

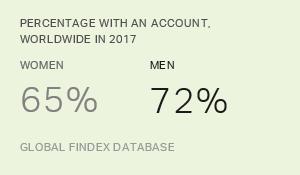

While there have been some advances in helping women gain access to financial services, globally, 65% of women have an account compared with 72% of men. The gender gap is similar in developing economies, with 67% of men and 59% of women having an account. There is no discernable gender gap in high-income economies.

The picture is not entirely bleak in developing economies. Consider India, where a strong government push to increase account ownership through biometric identification cards helped narrow both the gender gap and the gap between richer and poorer adults. And several developing economies have no significant gender gap, including Argentina, Indonesia and South Africa.

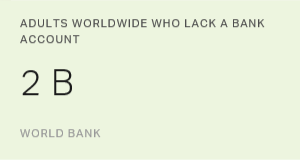

Still, women remain overrepresented among the world's unbanked. About 980 million do not have an account -- that's 56% of all unbanked adults globally.

This is true even in economies that have successfully increased account ownership and have a relatively small share of adults who are unbanked. In Kenya, for example, where only about a fifth of adults are unbanked, about two‑thirds of them are women. Women make up nearly 60% of unbanked adults in China and India -- and an even higher share in Turkey. Things are not much different in economies where half or more of adults remain unbanked: in Bangladesh 65% of unbanked adults are women, and in Colombia, 56% are.

Majority of Unbanked Women Are Out of the Labor Force

Using Gallup World Poll data on labor force participation, the Global Findex shows that account ownership is closely linked to employment status. In developing economies, 78% of adults who work for an employer have an account. For those who are out of the workforce, the share is just 53%.

One possible reason why women are heavily concentrated among the unbanked is their relatively low labor force participation. Overall in developing economies, World Poll data show women are twice as likely as men to be out of the workforce.

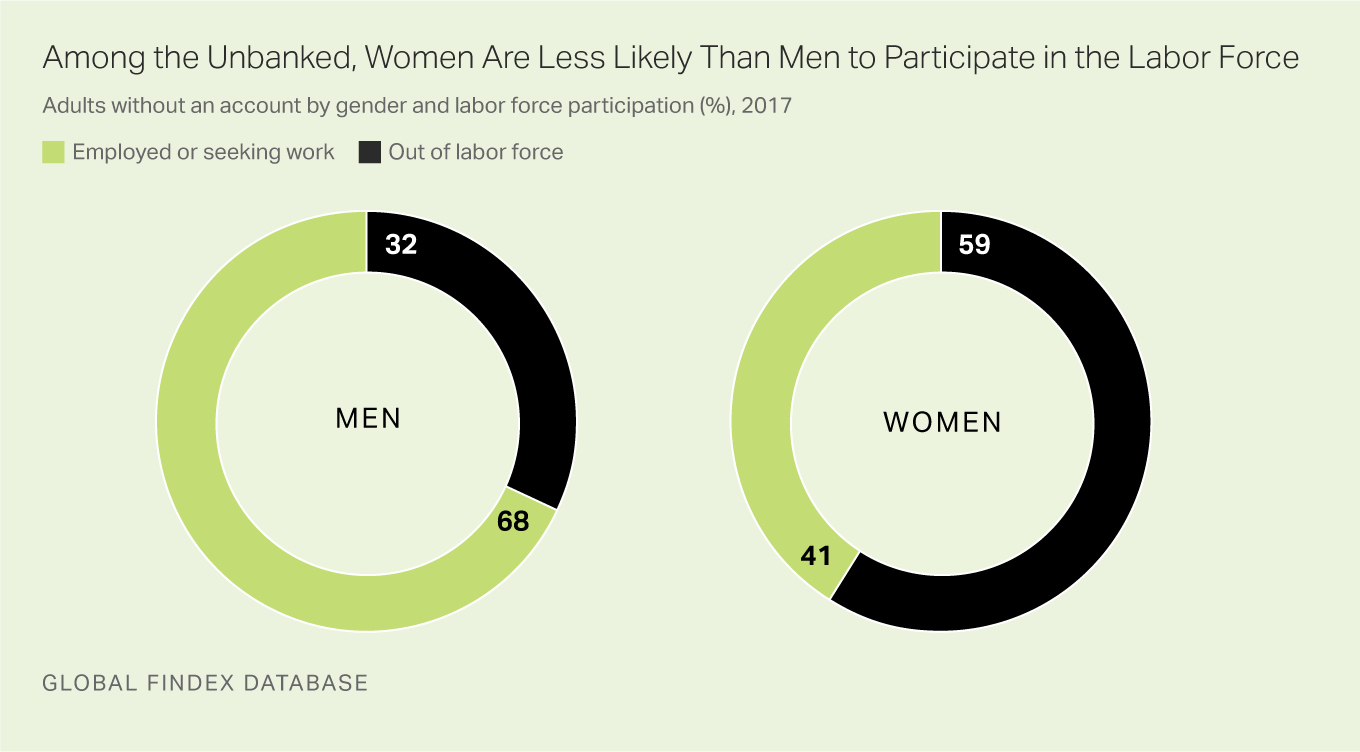

Gender differences in workforce participation extend to the unbanked. While 68% of unbanked men have a job or are looking for work, 59% of unbanked women are out of the labor force altogether.

Among unbanked adults who are economically active, self-employment is the most common form of work. Indeed, more than a quarter of all unbanked adults reported being self-employed, while less than a fifth reported working for wages. The reverse is true for adults overall in the developing world: the share working for wages, at 31%, is slightly larger than the share who are self-employed.

Mobile Accounts Could Open Doors for Women

Beyond labor force participation, women face an array of obstacles to getting financial services, including discriminatory laws and conservative social norms. Simple accounts accessed through mobile phones might help thwart some of these barriers. Mobile money accounts are often easier to open than traditional bank accounts and they have the added benefit of allowing women to transact from the safety and comfort of their homes.

Consider the eight economies where 20% or more of adults have a mobile money account only: Burkina Faso, Ivory Coast, Gabon, Kenya, Senegal, Tanzania, Uganda and Zimbabwe. These economies all have a statistically significant gap between men and women in the overall share with an account as well as in the share with both a traditional bank account and a mobile money account. But just two of them -- Burkina Faso and Tanzania -- have a gender gap in the share owning a mobile money account only. The other six have no such gender gap.

Implications

While some economies made gains in account ownership since the previous Findex survey -- 515 million people gained access to accounts in the past few years alone -- the gains could have been even greater if women were sufficiently included. More inclusive growth in account ownership could have led to faster overall progress.

It is still too early to say whether and how mobile money accounts may help close the gender gap. More data is needed to truly understand any connections between mobile money accounts and gender inequality in account ownership. However, the gender-balanced results for mobile money in some countries so far suggests growing access to the technology may help.