This article is the first in a two-part series on global financial inclusion based on data collected for the World Bank Global Financial Inclusion (Global Findex) database.

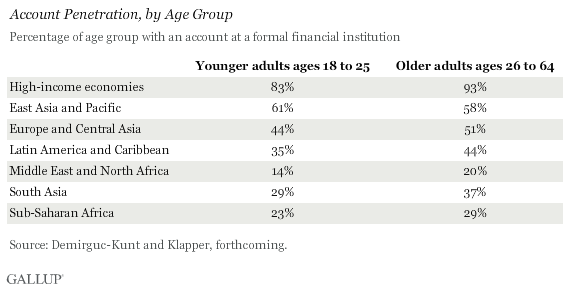

WASHINGTON, D.C. -- Younger adults in high-income and developing economies are considerably less likely than older adults to have an account at a formal financial institution. This age gap is evident in most world regions -- except East Asia and the Pacific -- as well as across income, gender, and education groups within economies.

These results come from a global study of financial inclusion, which measures how adults in 148 countries and areas save, borrow, make payments, and manage risk. The findings reflect more than 150,000 interviews with adults, aged 15 and older, and conducted in 2011. Gallup collected the data for the World Bank Global Financial Inclusion (Global Findex) database, which is funded by the Bill & Melinda Gates Foundation.

Account penetration among young adults -- defined as having an account at a bank, credit union, a cooperative, post office, or microfinance institution -- is 83% in high-income economies, compared with 38% in developing economies. The relative age gap in financial behavior is particularly big in the Middle East and North Africa, the region with the largest share of unbanked adults worldwide. In this region, young adults are 30% less likely to have an account than their older peers.

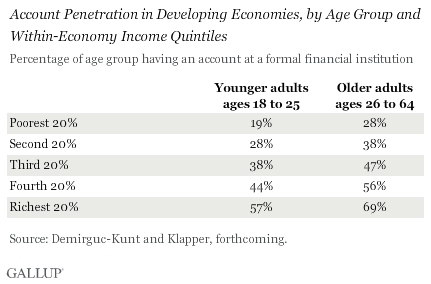

In the developing world, the age gap persists across income quintiles. In other words, even among the richest 20% of the population, youth are more likely to be unbanked than older adults.

Gender Gap Smaller Among Younger Adults

While women, the poor, and residents of rural areas in the developing world are usually less likely than their socio-demographic counterparts to have a bank account, with income held constant, the gender gap is smaller among younger adults. Women aged 26 to 64 are 18% less likely to be unbanked than men. Among 18- to 25-year-olds, the gender gap decreases to 14%. Because men are usually more likely than women to join the workforce, they are also more likely to open a bank account. Greater gender equality among younger generations might also be an explanatory factor.

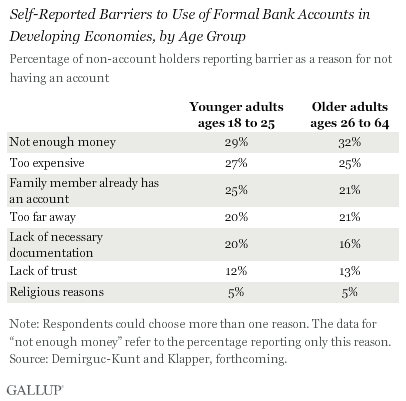

Lack of Money No. 1 Reason for Being Unbanked

Like older adults, the great majority (67%) of the 700 million unbanked young adults in the developing world say the reason for not having an account is the lack of money to use one; 29% cite it as the only reason for not owning an account. The second most cited barrier (27%) among unbanked youth is the high cost of bank accounts. Furthermore, 24% of the unbanked youth report that a family member already has an account. Lack of necessary documentation is a bigger barrier for youth compared with older adults, possibly because they are less likely to have official records in their own name such as a lease or home deed for residency requirements or a motor vehicle license as a valid government issued ID.

Younger Adults Less Likely to Save and Borrow

On a global level, formal saving and borrowing are also less prevalent among young adults. Eighteen percent of 18- to 25-year-olds report having saved money in the past year by using a bank, credit union, or microfinance institution, compared with 25% of 26- to 64-year-olds. This age difference is considerably bigger in developing countries than in high-income countries.

Furthermore, 6% of young adults and 11% older adults say they have borrowed money from formal financial institutions during the same period. However, no significant age gap was observed regarding informal borrowing behavior, that is, money borrowed from family or friends.

Implications

The Global Findex database enables leaders worldwide to evaluate the success of their financial inclusion policies that are specifically targeted at youth. Leaders and researchers are also encouraged to use the data to gain deeper insights of younger adults' saving, borrowing, payment, and risk management habits.

The data clearly identify the barriers to account use the 700 million unbanked youth in developing countries face. The biggest challenge will be to create enough good jobs that provide young adults with enough money to actually use a formal bank account. However, removing some of the other frequently reported barriers to having bank accounts such as high cost, physical distance, and lack of proper documentation would almost certainly be a good start to boost financial inclusion among younger generations. Expanding mobile banking systems seems to be the key in this endeavor.

Access the complete country-level data set, report, and questionnaire at www.worldbank.org/globalfindex.

For complete data sets or custom research from the more than 150 countries Gallup continually surveys, please contact us.

Survey Methods

Results are based on telephone and face-to-face interviews with more than 150,000 adults, aged 15 and older, conducted in 2011 in 148 countries and areas. For results based on the two age groups on the global level the maximum margin of sampling error is ±2 percentage points. The margin of error reflects the influence of data weighting. In addition to sampling error, question wording and practical difficulties in conducting surveys can introduce error or bias into the findings of public opinion polls.

For more complete methodology and specific survey dates, please review Gallup's Country Data Set details.

Demirguc-Kunt, A., and L. Klapper. Forthcoming. "Measuring Financial Inclusion: The Global Findex Database." Brookings Papers on Economic Activity.